Self-Invested Personal Pension

Switch your pension on. Switch your future on.

What is a SIPP?

A Self-Invested Personal Pension (SIPP) is a type of account that allows you to take charge of your retirement savings. You have the freedom to invest exactly where you want to and control how much money goes in and when.

You have all the same tax advantages as a traditional pension, and the government will still give you a boost of up to 45% (or 48% if you're a Scottish rate tax payer) on top of anything you pay in as tax relief.

You can even use a SIPP to combine all your old pensions into one easy-to-use online account. And take money out from age 55 (rising to 57 from 2028).

Pension and tax rules can change and any benefits will depend on your circumstances.

This video explains the features and rules of a SIPP (Self-Invested Personal Pension), including tax benefits and pension income options.

Join over 500,000 clients already using the HL SIPP

- Flexible payments - Monthly direct debits from as little as £25 a month, with the ability to pause or cancel payments if you ever need to.

- Invest where and how you want to - You can pick your own investments, select one of our ready-made portfolios, or pay a financial adviser to choose investments for you.

- Freedom at retirement - With the HL SIPP, you're free to choose from all the main retirement options.

HL READY-MADE PENSION PLAN

A new investment solution which will make starting a pension even easier.

SIPP charges

The HL SIPP is free to set up and low cost to run. Our yearly charge for holding investments is never more than 0.45%. Some investments will have their own annual charges, so please check these first before you invest.

It’s free to buy and sell funds. Other dealing charges depend on the type of investment and how often you trade.

How to top up your SIPP

Make a one-off lump sum payment from £100 or more. Please read the Key Features (including contribution checklist) first, then:

1. Log in to your account online or through the HL app

2. Select your SIPP account and choose 'Add money'

3. Follow the debit card instructions

HL READY-MADE PENSION PLAN

Don't know where to invest your pension? We’ve got a new investment solution which could help.

Add a little, build a lot

The power of regular investing

Invest from as little as £25 a month by direct debit.

- It's good discipline - it stops knee jerk decisions, and removes the temptation to try and time the market.

- You'll benefit from 'pound-cost averaging' - investing automatically helps smooth out the bumps in the market, spreading your money across different market conditions.

- Share buying is free - there’s no fee if you buy shares through direct debit, compared to £11.95 for lump sums.

How much should I invest?

Your results

About this calculator: This calculator is an example - it doesn’t show what your investments will actually be worth. And doesn't include any pension tax relief that you may receive. Investing is best considered for the long term (5 years or more). Remember investments can go down as well as up in value so you could get back less than you put in.

To make these calculations, we've included an annual charge of 1.25%, but this could be lower or higher, depending on the investments you hold. We haven’t factored in inflation. These results are based on a growth rate of 5%, unless you have adjusted the growth rate in 'Additional options'.

Pension contributions

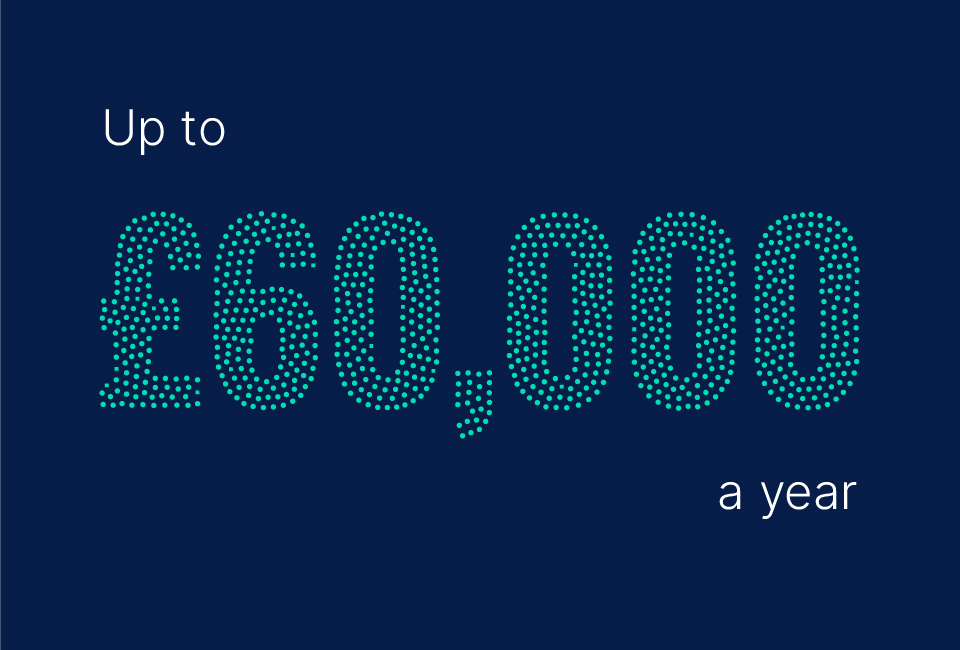

Most people can invest up to £60,000 into their pension each tax year. This can vary depending on your earnings. Even if you've accessed your pension, future contributions may be possible.

Transfer a pension

Moving old pensions to your HL SIPP can help you to take control of your retirement savings.

Investment ideas

Learn about different strategies for investing a pension, plus fund ideas for income and growth.

Employer contributions

Make an employer contribution to your HL SIPP on behalf of your own company. Or add money to an employee's HL SIPP.

Withdrawing money

You can usually access your pension from age 55 (rising to 57 from 2028), and choose between guaranteed and flexible income options.

Two simple ways to open a SIPP

Start with a bank payment

Set up monthly payments from as little as £25, or make one-off payments of £100 or more.

You can change your pension contributions whenever you like.

Transfer your old pensions

Transferring pensions from another provider, including old workplace pensions, can help you to take control of your retirement savings.

The fastest way to transfer is online.

The HL SIPP allows me to buy and sell investments with ease, particularly through the app which is excellent. I made sure that my pensions weren’t scattered around with different providers, and I consolidated them into one account for convenience and easy management. Keeping things simple and together, I believe, has enabled me to make better investment decisions.

How much can you pay into a SIPP?

If you're a UK resident under 75, you can usually pay in as much as you earn each year, up to £60,000 across all your pensions, and get tax relief. You may be able to pay in more or less than this amount if you have unused allowance from previous tax years, you're a high earner or have flexibly accessed your pension.

What can I invest in with a SIPP?

With a SIPP, you’re in control of how and where you invest.

To build your own portfolio, choose from over 2,500 funds, UK and overseas shares, investment trusts and more. Or, you can choose from a range of ready-made options where our team of experts will take care of the day-to-day investment decisions for you.

Taking money from a SIPP

Money in your pension is usually locked away until you’re 55 (57 from 2028). But any time after that, you can start to withdraw money, even if you’re still working.

Use your SIPP to buy a guaranteed income for life, or keep it invested and make withdrawals as and when you need to. Plus, get up to 25% tax-free (all other income withdrawals are taxable).

YOUR PENSION IN

YOUR POCKET

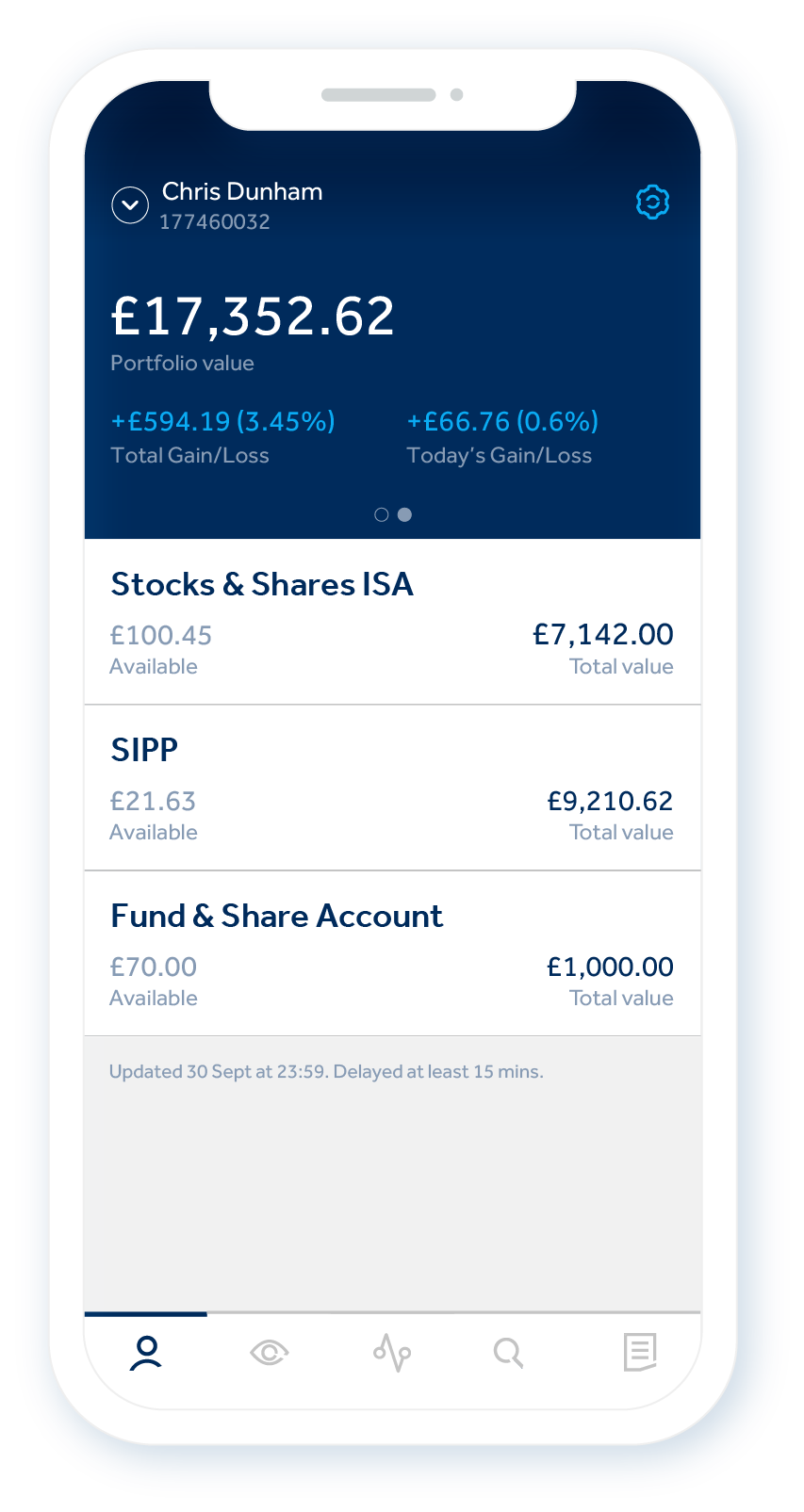

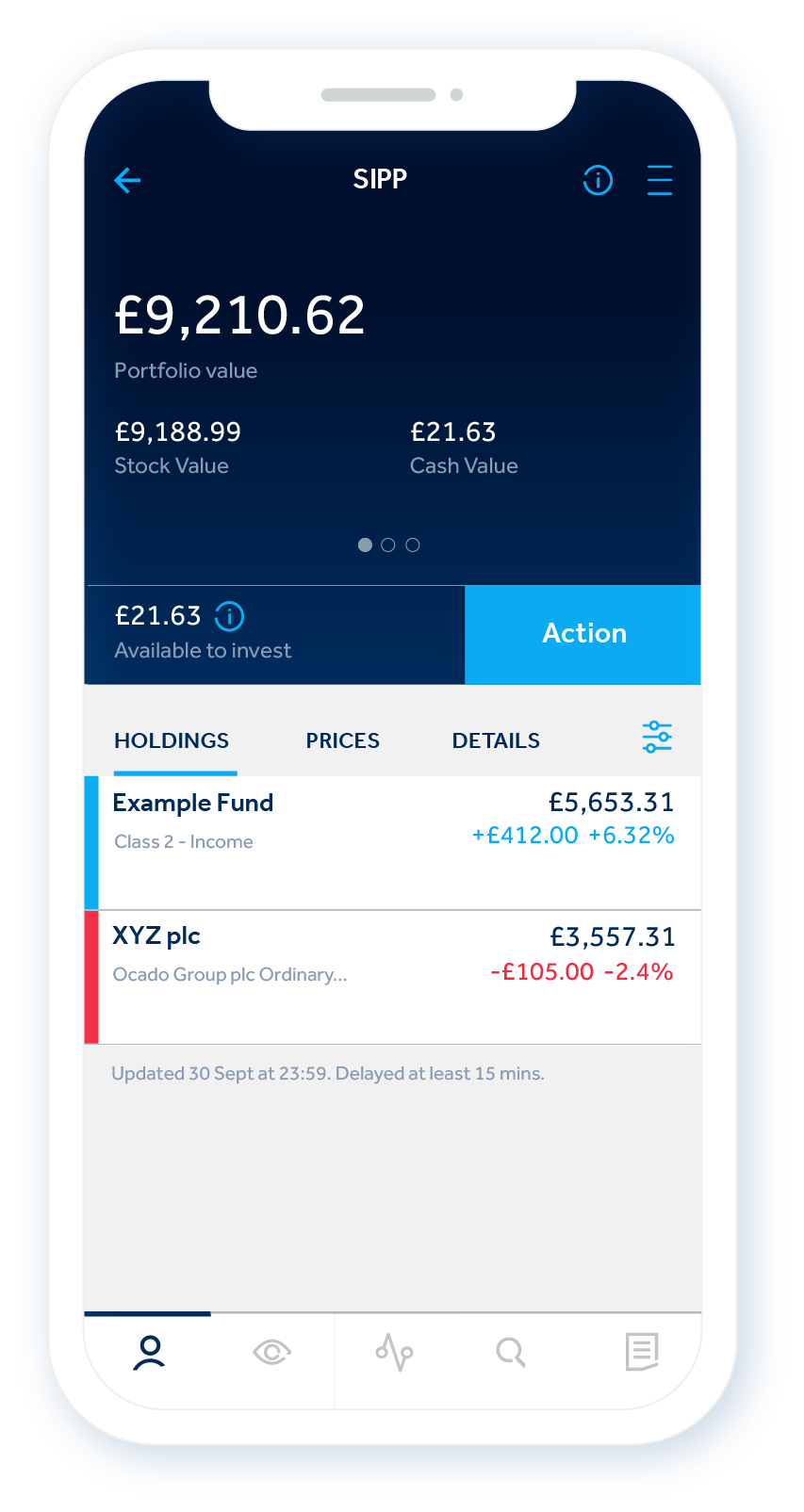

The HL app

-

Fast, secure account access

Log in to your account securely using fingerprint login and Face ID on iPhone.

-

Your investments at a glance

It's easier than ever to see your investment performance and if your pension's on track.

-

Place deals on the go

Buy and sell investments, even on the move.

Apple, the Apple logo, Face ID and iPhone are trademarks of Apple Inc., registered in the U.S. and other countries.

Apple, the Apple logo, Face ID and iPhone are trademarks of Apple Inc., registered in the U.S. and other countries. App Store is a service mark of Apple Inc., registered in the U.S. and other countries. Android, Google Play and the Google Play logo are trademarks of Google Inc.

SIPP Account FAQs

SIPP FAQs

Boring Money Awards 2024

Boring Money Awards 2024

The Personal Finance Awards 22/23

Help and support

If you have any questions about the HL SIPP, you can speak to one of our UK-based client support experts.

Call us on 0117 980 9926

Switch your pension on

Helping people save and invest for over 40 years

Trusted by 1.8 million clients

We’re a financially secure FTSE-listed company, authorised by the Financial Conduct Authority. And have won over 200 awards.

Expert knowledge and guidance

Get the latest investment news, research and insight. Plus tools to help you make decisions with confidence.

Ongoing support

Help from our UK-based client support team. Or personal financial advice from our highly qualified experts.