How to build a portfolio

We take a closer look at how to build an investment portfolio with the right mix of assets, known as asset allocation.

Important notes

This article isn’t personal advice. If you’re not sure whether an investment is right for you, please seek advice. If you choose to invest, the value of your investment will rise and fall, so you could get back less than you put in.

Learn about investing

Before you start investing, you’ll need to think about your strategy.

Your investment strategy should be one that matches your objectives and risk appetite, and aims to achieve the best return for your chosen level of risk.

We take a closer look at asset allocation and set out the four steps to build your own personalised portfolio from scratch.

This article isn’t personal advice. If you’re not sure what’s right for your circumstances, our financial advisers can help. All investments can fall as well as rise in value, so you could get back less than you invest.

What is asset allocation?

It’s a term that might sound confusing, but it’s simply a strategy for investing.

It’s all about building your investment portfolio to align with your objectives, risk appetite and target returns. This is achieved by investing in a mix of asset classes like shares and bonds.

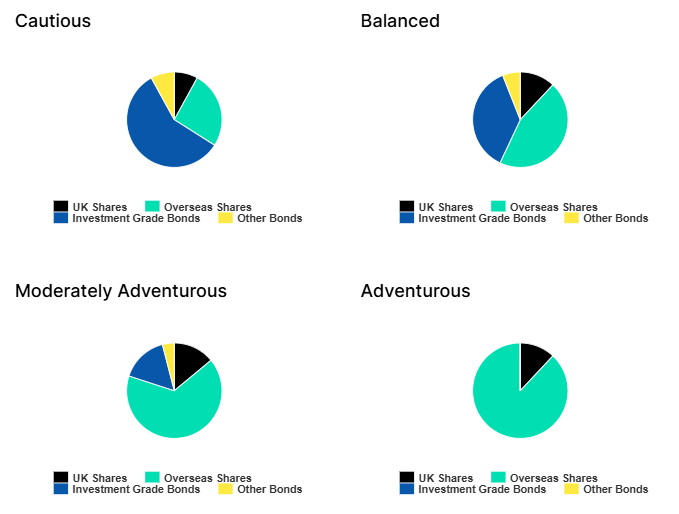

Below you can see some examples of how your portfolio might look, from a cautious portfolio to an adventurous one. These portfolios do not consider cash, however it’s important to build up an emergency savings pot before you start investing.

Once your portfolio is built, you’ll need to regularly rebalance it back to its original weightings and risk level. We’ll explain more about this later.

If your circumstances change, we’d recommend reviewing your investment strategy and objectives. All investments should be held for the long term too – that’s at least five years.

Ready-made investments

Leave it to the experts with our all-in-one funds.

What are the different types of assets?

Broadly speaking, assets can be split into three main categories – shares, bonds and alternatives like gold. And while there are lots of ways to define an asset class, it’s their characteristics which really matter.

Investments in an asset class are broadly similar to one another. For example, UK shares are one asset class. They all give investors part-ownership of a company and are listed and traded on the London Stock Exchange.

We can separate asset classes by looking at what’s different from one to another. UK corporate bonds aren’t listed on the stock exchange and don’t provide investors with ownership of the company. They pay out a fixed income, while dividends from shares can vary and aren’t guaranteed. It’s these kinds of differences that make shares and bonds two separate asset classes.

Lastly, the addition of an extra asset class to a portfolio should offer the potential to improve the expected return for the same level of risk – allowing you to get the most reward from your risk. This is an important characteristic for an investment strategy, and is why diversification is often championed by many investors.

Diversification is the only free lunch [in investing]

Nobel Prize Winner Harry Markowitz

Time to start thinking strategically

Here are the four steps you need to take to create a portfolio that’s right for you.

1. Know your objectives

It’s important to know what you want to achieve by investing. This might seem like an obvious thing to say, but it’s something that can go under the radar.

For most of us, we invest with a common goal: to improve our financial future and give us an income in retirement. But you could also have other key milestones along your investment journey that you need to plan for. Things like building a house deposit, or contributing towards your children’s university fees.

Knowing your objectives will paint a clear picture on your investing time horizons and the level of returns you're aiming for. This, as well as your risk appetite, will help shape the overall risk profile of your portfolio.

2. Choosing your risk

Risk is personal. The person best placed to decide how much risk to take is you.

Choosing your level of risk can be a difficult decision though. To help, it should mostly be about your long-term financial needs and not based on your short-term views of the market. Your strategy and mindset should also be robust enough to withstand the market ups and downs. Remember a financial adviser can act as a fresh pair of eyes and help you make the right call.

As a general rule, investors who are many years away from retirement can afford to take greater risks by investing more in shares. For those approaching retirement, it’s sensible to gradually lower the amount invested in shares by increasing their exposure to bonds, which typically offer less fluctuation in returns.

It’s important to remember though, on average, we live for over two decades after stopping work, so lots of us should continue to hold some shares well into our retirement.

3. Selecting your assets and investments

Picking the right mix of shares and bonds is arguably the most pivotal part of the process.

Shares are riskier investments than bonds. But if you’re looking to grow your money or haven’t yet saved enough to meet your financial needs, you should consider taking more risk to try and achieve the higher returns which will help you reach your goals.

Greater risk means greater volatility though, so you’ll need to be comfortable with the market ups and downs you could experience along the way.

On the other hand, high quality bonds tend to give a relatively predictable and secure source of income. Of course, past performance isn’t a guide to the future. This can make them a sensible option for a larger part of an investment portfolio if you’ve already built a sizeable retirement pot, for example.

Getting your share-to-bond ratio right is the most important part of your investment strategy.

The second most important is to diversify.

The benefits of diversification exist because your portfolio is exposed to different types of risks. For example, investing in shares in developed markets comes with different risks to investing in shares in emerging markets.

Once you have decided your asset weights, you’ll need to select investments within each asset class. For any one investment, risk and return are two sides of the same coin. But when we combine investments, it’s possible to lower expected risk without sacrificing expected returns. Before you invest, make sure you understand the specific risks of the investment.

By investing in a mix of asset classes – and various equities and bonds - across different countries, industries and companies, you’ll be best placed to reap the rewards of diversification.

4. Maintaining your asset allocation

To help keep your portfolio on track to meet its objectives, you’ll need to make sure it’s rebalanced regularly.

Rebalancing involves selling a little of what’s done well and reinvesting elsewhere – assuming your risk level and objectives haven’t changed. That way, you will stick to your strategy, keeping the ratio of different asset classes in your portfolio steadier over time.

Sometimes that’ll mean selling bonds and buying shares, and sometimes it’ll mean doing the opposite. In some cases, you might also want to rebalance between individual holdings. If one of your investments does especially well, it might become a larger portion of your portfolio than you initially intended.

To recap, here is the four step checklist to building and maintaining your own portfolio:

Know your objectives

Choose the right level of risk

Select your investments within each asset

Rebalance your portfolio and review your strategy

Putting principles into practice

Understanding your investment strategy is one thing. Sticking to it is another.

In times of uncertainty, it’s important for investors to hold their nerve and think long term. History tells us market falls have tended to happen around every 5-10 years, but it’s impossible to predict exactly when they will happen. By selling your investments after they’ve fallen in value, you miss out on the potential for them to bounce back when prices eventually recover.

And while we don’t know what’s around the corner, we do know investing for the long term, and sticking to your game plan offers investors the best chance of achieving their goals and securing a better financial future.

Ready to start investing?

We can help. There are different levels of support we offer to help you build your portfolio. This can be through guidance or advice.

Guidance

You’ll be responsible for making sure the decisions you make are right for your individual circumstances and your needs.

We’ll give you clear information and tools to help you make decisions to improve your financial health, including:

The Wealth Shortlist – Our Wealth Shortlist has a list of funds which is designed to help our clients select their investments and build a diversified portfolio. Funds are a collection of investments which are chosen and run by a professional fund manager, so you’ll benefit from the manager’s knowledge, expertise and research into lots of different companies.

Ready-made portfolio – Building your own portfolio from scratch isn’t right for everyone – you’ll need the time and know-how to do this. For a more hands-off approach, why not leave it to the experts by investing in a ready-made portfolio?

Advice

We’ll be responsible for making personal recommendations that are suitable for your needs and circumstances.

Financial advice – Not everyone has the time or motivation to choose their own investments. If you don’t fancy doing things yourself, you could consider paying a qualified and regulated HL financial adviser to help you.

As a rule, if you’re not sure whether an investment is right for you, you should ask about financial advice. You’ll just need to make sure the information you provide to your HL adviser is as accurate and up to date as possible.