Self-Invested Personal Pension (SIPP)

Open a SIPP with the UK's most popular provider

Invest your way with a wide choice of funds, shares, ETFs and more.

Leave it to the experts with our Ready-Made Pension Plan, free until May 2027 for new SIPP clients. Offer ends 31 July 2026. Terms apply.

Combine old workplace pensions in minutes into our award-winning Self-Invested Personal Pension.

Before you invest in a SIPP: investments usually outperform cash savings over 5+ years. But values rise and fall, so you could get back less than you invest. You’re responsible for your investment decisions. Pensions are designed to help fund retirement, so money can’t usually be taken out again until at least 55 (rising to 57 in 2028). Pension and tax rules may change, and benefits depend on your circumstances. Scottish tax bands and rates are different, and different benefits apply. Before you transfer a pension check for loss of benefits, guarantees and exit fees.

Before you invest in a SIPP: investments usually outperform cash savings over 5+ years. But values rise and fall, so you could get back less than you invest. You’re responsible for your investment decisions. Pensions are designed to help fund retirement, so money can’t usually be taken out again until at least 55 (rising to 57 in 2028). Pension and tax rules may change, and benefits depend on your circumstances. Scottish tax bands and rates are different, and different benefits apply. Before you transfer a pension check for loss of benefits, guarantees and exit fees.

What is a SIPP?

A Self-Invested Personal Pension (SIPP) gives you control over your retirement savings. They offer generous tax benefits (like workplace pensions) and the ability to combine old pots. You can choose your own investments or leave it to experts with ready-made options.

Save tax

Enjoy similar tax perks to a workplace pension, with 20% - 48% tax relief on what you pay in until age 75.

Invest your way

Choose the expertly managed Ready-Made Pension Plan or pick your own investments.

Combine old pensions

Transfer old workplace pensions in minutes into one easy-to-use online account.

Our Ready-Made Pension Plan, now free until May 2027

Let our experts handle your investments, while you handle everything else.

New SIPP clients: invest by 31 July 2026, and we’ll cover your charges until 30 April 2027. Fund charges will be paid back into your HL account as cash. Terms apply.

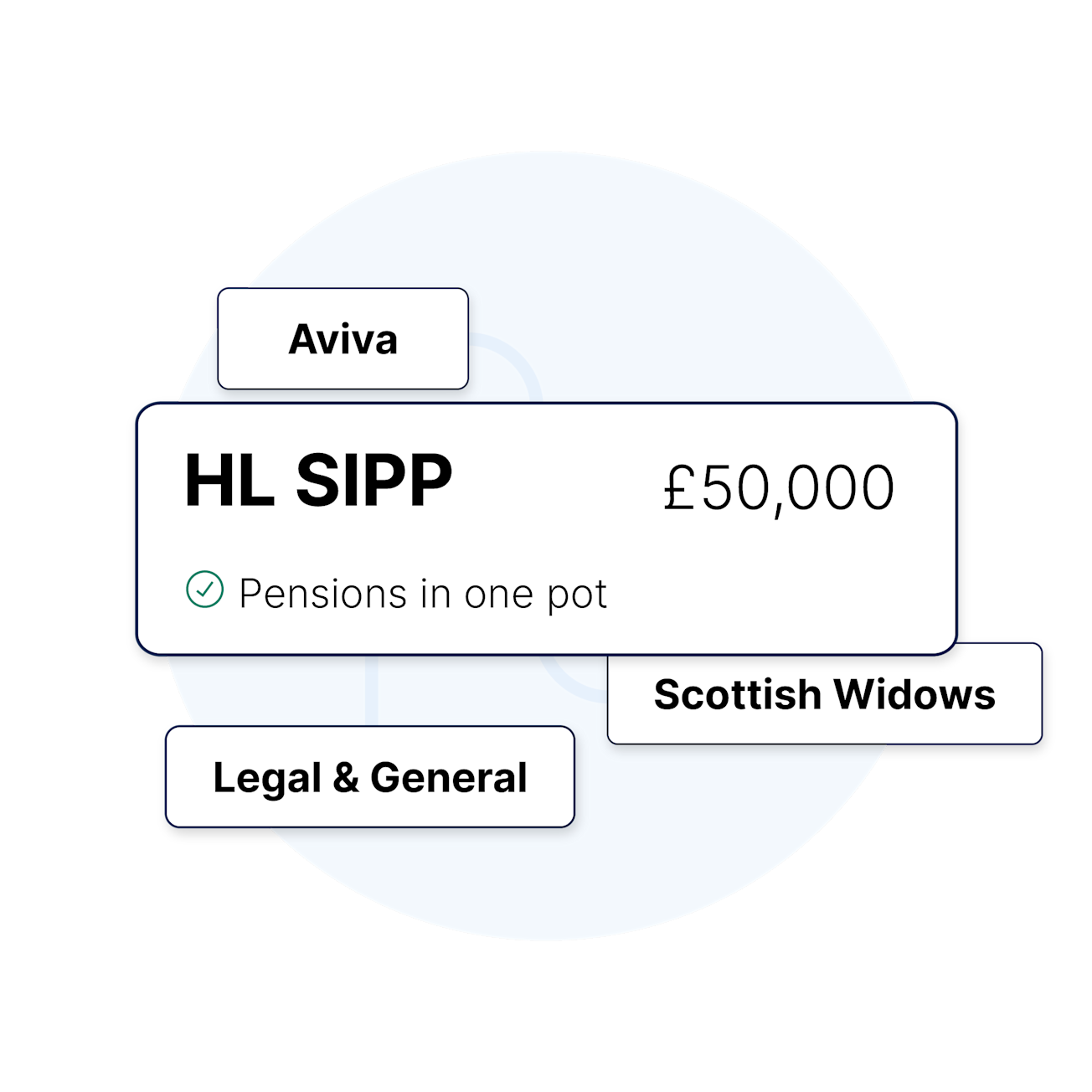

Combine old pensions in minutes

Have old workplace pensions with Aviva, Scottish Widows, or Legal & General?

Out-of-sight pensions can underperform. By transferring them into the HL SIPP, you can unlock higher returns and wider investment choice.

It only takes a few minutes to get started. Just tell us what pensions you’d like to transfer, and we’ll handle the rest.

Why choose the HL SIPP?

Enjoy wider investment choice, expert insights, and tailor your retirement income to suit your needs.

The UK’s most popular SIPP, now even better value.

Affordable regular investing - pay no dealing charge when you invest monthly.

Let our experts manage your investments with the Ready-Made Pension Plan

See your pension in one tap with our award-winning app.

Regular investing: easy and affordable

Pay no dealing fees when you invest monthly. Just set your monthly amount, pick your fund, share, or ETF, and we place your trades automatically.

No set up fees

No charge to buy investments, but some investments may have their own charges

Simple, automatic monthly investing

No minimum amount to open your SIPP

There’s no minimum amount to open a SIPP with us.

You can add as little or as much as you like - giving you complete flexibility from day one. You can stop or change your contributions at any time.

Why clients choose the HL SIPP

Meet Julie, our first ever SIPP client.

"One of my values is independence and flexibility. I needed a pension that would tick those boxes. The HL SIPP did that for me."

Meet Julie, our very first Self-Invested Personal Pension (SIPP) client, as she shares her inspiring journey of saving for retirement with HL.

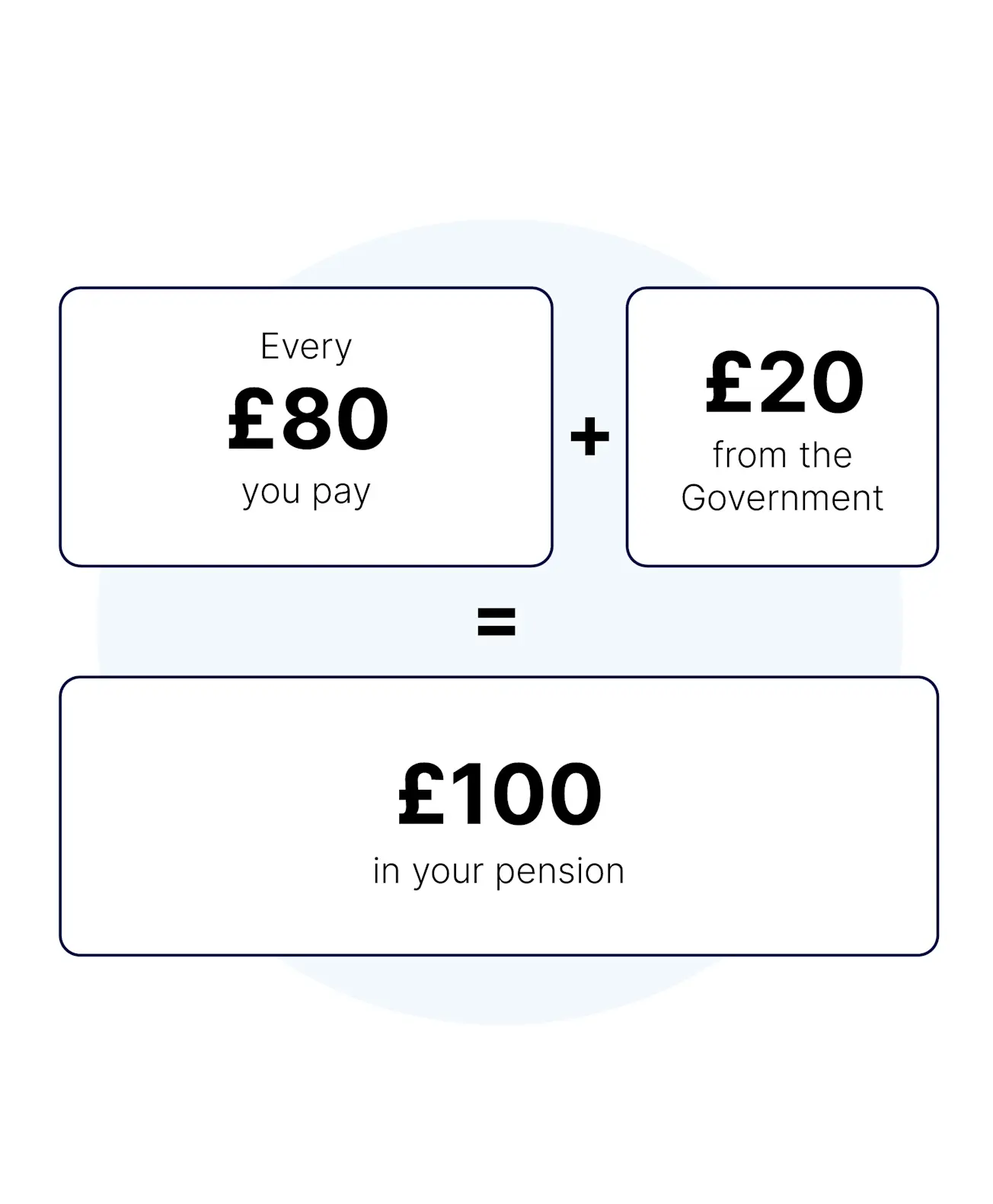

How does pension tax relief work?

When you pay into your pension, the government adds at least 20% in pension tax relief to your contribution.

Meaning for every £80 you put in, the government adds £20 making your total contribution £100.

If you’re a higher or additional rate taxpayer, you could claim 40% - 48% tax relief through your tax return.

Pension and tax rules can change, and benefits depend on your circumstances. Contribution limits apply. Money in a pension is usually accessible from age 55 (57 in 2028).

Is a SIPP the right choice for you?

Anyone can open a SIPP, but it could be a great option if you:

Want to boost your retirement savings beyond your workplace pension.

Have old workplace pensions you’d like to bring together into one easy-to-manage account.

Are self-employed and want a tax-efficient way to save for retirement.

Are a higher-rate taxpayer looking to lower your tax bill.

Are comfortable choosing your own investments (if not, you can choose a Ready-Made Pension Plan).

This isn’t personal advice. If you’re not sure what’s right for you, ask for financial advice. Investments can rise and fall in value, so you could get back less than you invest. Tax rules can change, and benefits depend on your circumstances.

SIPP charges

0.35%

Free to open, with an account charge of no more than 0.35% for holding investments. The investments you choose may have their own ongoing charges.

Dealing charges apply for one-off trades.

FAQs

Here you'll find answers to the most frequently asked questions.

You can open a SIPP if you're:

Between 18 and 75 years old

A UK resident

A UK taxpayer (to benefit from tax relief)

You can open a SIPP whether you're employed, self-employed, or not currently working. There's no requirement to be employed – anyone can start a SIPP.

What do you need to open a SIPP?

You can set up an HL SIPP from as little as £25 a month, or by making a one-off contribution of £100 or more. All you need to hand is your National Insurance number and either your bank details or debit card.

You can also open a SIPP by transferring a pension. The fastest way to transfer is online. You'll need your pension name and type (e.g. Aviva personal pension), policy number and pension value (this doesn't have to be exact) to get started. You should be able to find these details on your annual statement or you can ask your current provider when you’re checking what exit fees apply or if you’ll lose any valuable benefits.

Yes, you can have both a SIPP and your existing workplace pension, and this can be a flexible way to top up your retirement savings tax-efficiently. If you have access to a workplace pension, make sure you’re maximising any employer contributions before deciding whether to pay into a SIPP.

You’ll also need to make sure the money put in across all your pensions each year (including any basic rate tax relief added by the government) doesn't go over the total pension annual allowance of £60,000.

You can hold multiple SIPPs, but there are important factors to consider. While it's possible to have more than one SIPP, managing all your pensions in one place is often simpler and more efficient. Keeping your pension funds consolidated allows for easier tracking and better control of your investments.

If you hold multiple SIPPs, you need to be mindful not to exceed the £60,000 pension annual allowance. It applies across all your pensions, including any workplace pensions.

Pensions are designed to help fund retirement, so you can usually access money in a SIPP from age 55 (rising to 57 in 2028). If you try to take your money out sooner, you may have to pay a penalty. There are circumstances under which you can access your pension early without a penalty. Speak to your SIPP provider or a financial adviser if you're unsure.

Do you have to pay tax on SIPP withdrawals?

Yes, you may have to pay tax on SIPP withdrawals.

25% of your pension pot can be taken tax free. The remaining 75% is taxed as income at your marginal rate, and added to any other income you've received in the same tax year.

For example, if you take a large withdrawal that pushes your total income above the basic rate threshold, the excess will be taxed at higher rates (20%, 40%, or 45%, depending on your total income).

Try our pension income tax calculator to see how your income might be taxed.

All of these retirement income sources are taxable:

A one-off lump sum (known as UFPLS)

An annuity (guaranteed income for life)

Withdrawals are added to your income for the year, so it’s wise to plan carefully to avoid moving into a higher tax bracket. Also, your first withdrawal may be taxed using an emergency tax code, which can lead to overpayment - though you can claim a refund from HMRC.

The pension annual allowance is set at £60,000 or 100% of your earnings, and this is the total value that can be paid into all your pensions each tax year before triggering a tax charge.

If you want to pay in more and you have unused allowances from the past three years, you may be able to do so.

If you have a ‘threshold income’ above £200,000 and an ‘adjusted income’ of more than £260,000, you will see your annual allowance reduce by £1 for every £2 of adjusted income over the £260,000 limit. This is called the Tapered Annual Allowance (TAA) and can be as little as £10,000.

Every UK resident under 75 qualifies for basic-rate (20%) tax relief on pension contributions, even children and other non-taxpayers. You can usually add whichever's highest out of the amount you earn, or £3,600, and receive tax relief each year. There is also an annual allowance (£60,000 for most people) which limits what you can pay in. Each contribution includes the money you put in, as well as what the government adds in tax relief.

This basic-rate tax relief is added to your pension automatically. Your pension provider claims it for you from the government and adds it to your pension.

If you pay higher-rate tax (40%) you can claim up to a further 20% in tax relief through your tax return or local tax office.

Top-rate taxpayers (45%) can claim back up to a further 25%. You must pay enough tax at the relevant rate to claim back the full amount.

If you’re a Scottish taxpayer the amount of tax relief you can claim is different. Take a look at our information on the Scottish income tax changes page.

Tax rules can change over time and the relief you receive depends on your circumstances.

We've won over 200 awards for our services