Investing in the stock market

Simple strategies for success

Important information - This page is designed as guidance, not personal advice. Learn more about the differences between the two. If you’re still not sure what’s right for you, you should ask for advice. All investments and any income they produce can fall as well as rise in value so you could get back less than you invest, especially over the short-term. Past performance is not a guide to the future.

You don’t need to be an expert in finance or be a doctor in economics to be a good investor.

What you do need is time, patience, and a rock-steady mindset.

Stock market highs and lows are part of investing. It can be an emotional rollercoaster at times. That’s why understanding how to invest, and what role human psychology plays, is an essential part of becoming a successful investor.

Here’s more on common investing behaviours and how to put yourself on the right track to reaching your goals.

The human side of investing

At a glance

It’s essential to have the same mindset and approach to investing if the market is rising, to when it’s falling in the short term. Stick to your strategy, even when things feel uncertain.

Markets usually recover and rise over the long term. We can often use what we’ve learnt from past drops in the market, like the 2008 Financial Crash or Covid-19 in 2020, to understand how markets have recovered over time.

Investing for at least 5-10 years gives you the best chance of success. Those who pick investments they think have the potential to do well over the long term are usually in the best position to be rewarded. Though as always with investing, there are no guarantees.

Speculating and trying to profit on small market movements is both hard to keep track of, but could also be costing you more than you think. This is from underlying charges like Stamp Duty and FX charges. Know the costs of every trade, as they could eat into your returns.

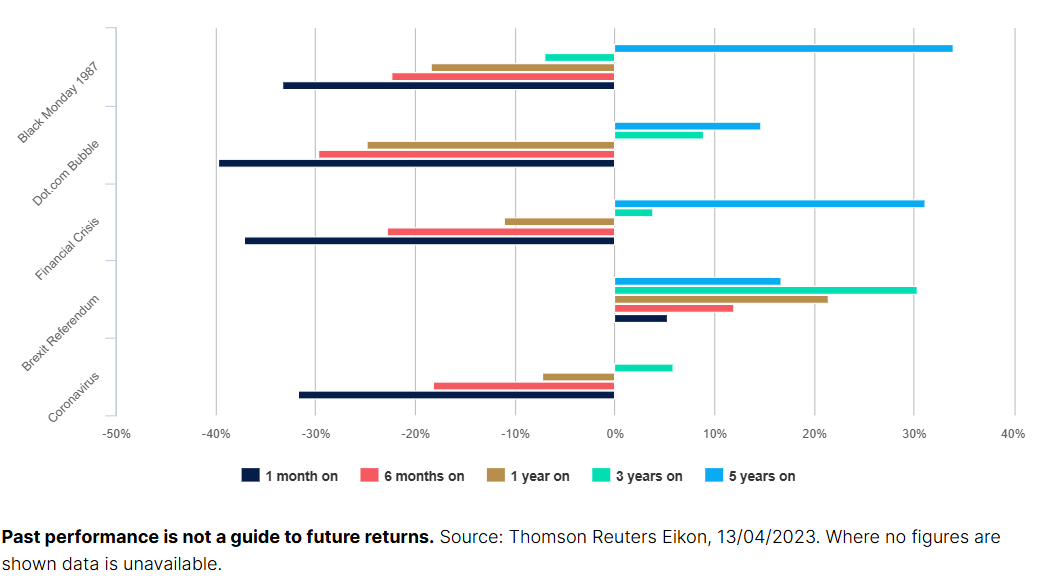

Every investor has to deal with the ups and downs of investing.

We’re emotional beings by nature – we’re thrilled when the market rises, but can panic when it falls.

Holding your nerve through the downturns can be hard to stomach. But history teaches us that markets have risen in the long term.

Here are some of the biggest falls in the UK stock market since 1985 and how long it took to recover. We’ve assumed you’d have invested at the highest point before it began to fall.

Clearly, the tough times don’t last forever. It’s essential to think long term and stay resilient, especially if markets feel uncertain.

Here are some investing dos and don’ts to bear in mind:

Do:

Find high-quality companies and investments at the right price that you can hold for a long time

Collect steady dividends or growth over the long term

Don't:

Jump in and out of investments to try and time the market

Be swayed by short-term price movements

Short-term speculation vs. long-term investing

Investing is a marathon, not a sprint.

Broadly, investors can be grouped into two camps – short-term speculators and long-term investors.

Speculators try and predict the market’s next steps. They’ll chop and change their investments trying to profit from the small changes in the market. Usually, their time horizons are a few months or even less. This can be very risky.

Long-term investors ignore the short-term hype and look two steps ahead, picking companies they think have the potential to perform well over five to ten years.

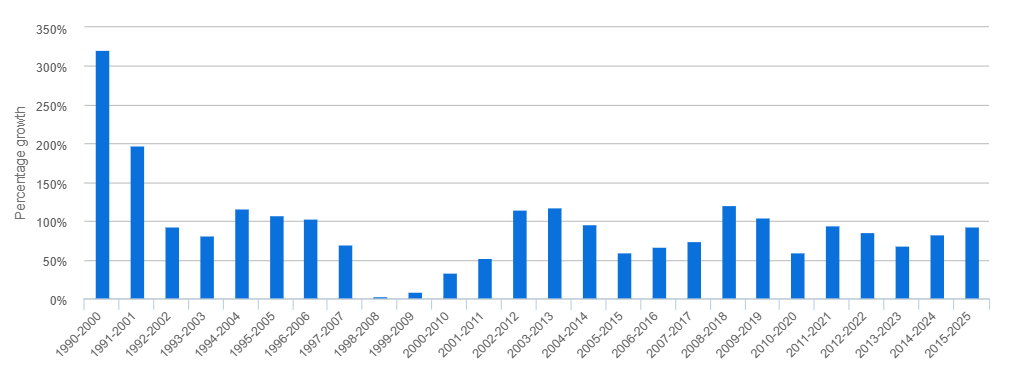

We think the best investments show their value in the long term.

This chart shows the 10-year rolling returns for the FTSE 100 index over the last 30+ years.

Past performance is not a guide to future returns. Sources: Refinitiv, Lipper IM, as of 31/12/2024.

| Dec 2019 - Dec 2020 | Dec 2020 - Dec 2021 | Dec 2021 - Dec 2022 | Dec 2022 - Dec 2023 | Dec 2023 - Dec 2024 | |

|---|---|---|---|---|---|

| FTSE 100 index | -11.5% | 18.4% | 4.7% | 7.9% | 9.7% |

Before charges or taxes, investors playing the long game (10 years in this case) were rewarded with profits in all the periods between 1990 and 2023. Even during the 2008 financial crisis.

The most valuable lesson is that investing for the long term gives you the better chance of success. Remember past performance isn’t a guide to the future.

Real costs of trading too much

Trading too often can affect the performance of our investment portfolios over the long term for a number of reasons:

Fees and charges

Dealing fees – you’ll pay your broker a dealing fee each time you buy and sell shares. See our dealing charges.

Government taxes or levies – when buying UK shares, you’ll normally pay 0.5% Stamp Duty on the value of the trade (excluding other charges).

Foreign Exchange (FX) – this is a charge to convert the currency if you’re buying or selling investments traded in a foreign currency. Although this will depend on who you invest with.

Bid/offer spread

This is the difference between an investment’s buy (offer) price and sell (bid) price. Investments that aren’t traded as much will often have a bigger spread – like shares in smaller companies. More frequently traded stocks, like FTSE 100 shares, can have a smaller spread.

Portfolio turnover

This measures how frequently a manager trades the investments in their fund. The higher the turnover rate, the higher the fees because of the trading costs. Actively managed funds tend to have higher turnover rates than passive (index tracker) funds. It’s essential to read the Key Investor Information Document (KIID) before you invest to understand these underlying costs.

These costs add up so make sure you know what you’re being charged.

Some other things to think about:

Reduced returns – frequent trading can use up your capital gains allowance quicker, increasing your tax charges.

Diversification – overtrading could mean you end up with more of your portfolio in riskier investments. Keeping it balanced is key.

Learn how to diversify your investments

Missed opportunities – trading a lot could mean you miss the best days in the market.

Strategies

At a glance

Before you place a trade, ask yourself these 3 questions – what are your investment goals, do you understand the company or investment, and are you aware of the costs?

Diversification is a number one rule for investing. In a sports team, you wouldn’t pick players who are good at the same thing. Building a team of investments is no different. By diversifying, you spread your money between different investment types to reduce the overall impact of risk when investing.

Funds give you access to lots of different asset types as an easy and convenient way to help diversify your portfolio.

Questions to ask yourself before placing a trade:

What are my goals for investing?

Think about why you’re placing the trade, and why now. Is your portfolio missing this type of investment and will it help your long-term goal?

Do I understand the details of the company or investment?

Do you understand what the company does and how they make profit (if at all)? If the share price dropped by 5% tomorrow, would that change anything for you? Do you think the company could grow and evolve in the future?

Am I aware of the costs?

Is the investment’s price good value for money, and how much will dealing charges, stamp duty or FX charges eat into the total trade?

Importance of diversification

Diversification is an investing essential to manage your risk. Investment risk is the market ups and downs (volatility) you’ll experience when you invest. If an investment is riskier, it’s typically more volatile.

You diversify your investment portfolio by spreading your money between different types of investments, like shares or bonds, or different countries and sectors, to reduce the overall impact of risk when investing.

Picking individual companies isn’t always the answer to start diversifying – it’s not the easiest way. Investing in an individual company isn’t right for everyone because if that company fails, you could lose your whole investment. If you can’t afford this, investing in a single company might not be right for you. You should make sure you understand the companies you’re investing in and their specific risks. You should also make sure any shares you own are part of a diversified portfolio.

But an alternative investment option is funds, where professional fund managers make the underlying decisions and choose a selection of investments. Either way, it’s important to regularly check in on your investments to ensure they still meet your objectives and attitude to risk.

Funds – trusting the experts

Funds offer an easy and convenient way to invest and are popular with novice and experienced investors alike. They offer a simple way of diversifying across a number of different investments, and access to the skills of a professional fund manager.

A fund pools together the money of lots of different investors, and a fund manager invests on their behalf. Funds can invest in various types of assets like shares, bonds or property, depending on the investment objective of the fund.

Investing in funds isn’t right for everyone. You should only invest in funds if you have the time and know-how to diversify your portfolio to help reduce risk.

Before investing it’s important to check the fund’s objectives align with your own, understand the fund’s specific risks and if there’s a gap in your portfolio for that type of investment.

When’s the right time to start investing?

At a glance

Make sure you have enough emergency cash savings covering at least 3 months’ worth of essential expenses in an easy access account before you invest. How much exactly depends on your circumstances.

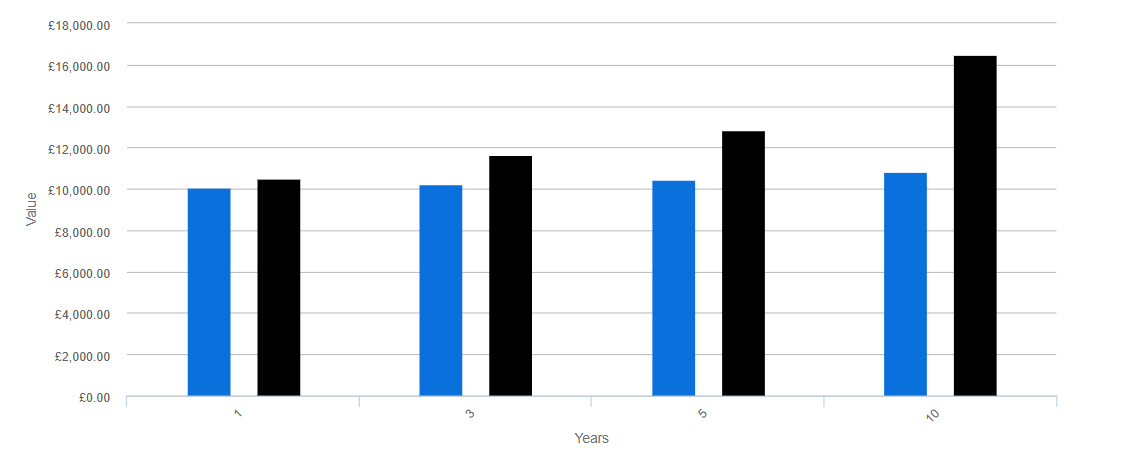

Other than your emergency cash savings, for any money you do not need in the next 5 years, investing tends to offer better returns over the long term than just holding cash.

You can see from the chart how we would expect the global stock market to perform against cash over the next 10 years. This is based on an initial £10,000 lump sum investment and does not include charges.

Time in the market is much more important than trying to time the market. We think at least 5 years as part of a diversified portfolio. This helps to smooth out any ups and downs and gives you the best chance of growth. As always with investing, there are no guarantees.

Source: HL. Based on market expectations as of 30 June 2024. For illustrative purposes only and not intended to serve as an accurate guide to future returns.

Time in the market not timing the market

There’s rarely a bad time to invest.

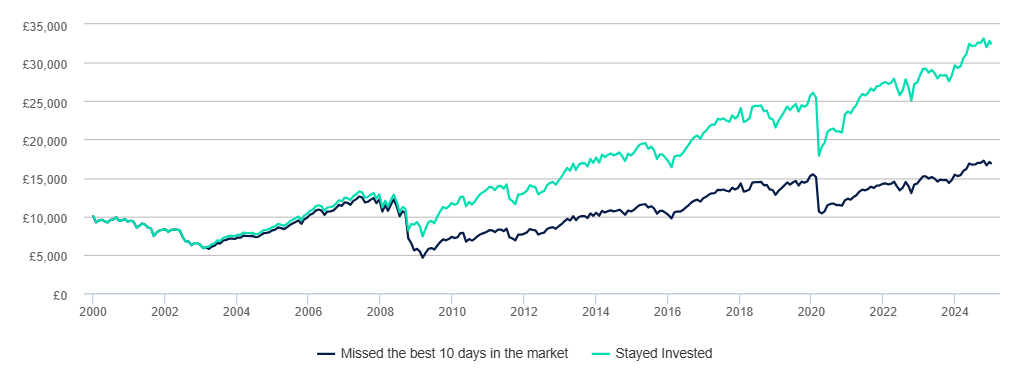

It’s all about playing the long game. That’s at least 5 years – ideally longer. If you stand on the sidelines, you can easily miss the most profitable days of investing.

Taking a long-term approach will help cut through the short-term noise of market movements and any worries about when’s the best time to invest.

Past performance isn't a guide to future returns. Source: Lipper IM, from 03/01/2000 to 31/12/2024. Figures based on £10,000 starting investment and do not take into account inflation or charges.

The chart above shows how missing the best days in the market can cost investors thousands. You would’ve been unlucky to miss them all, but is it a risk worth taking?

Which way the market moves short term doesn’t really matter. What does, is staying invested and diversified across areas you think will perform well over the next five to ten years.

Is cash really king?

Cash often seems the safest option. Technically it is. Unlike investments, the amount of cash doesn’t change.

But it isn’t totally risk free.

Inflation is the cost of things we buy every day rising – it reduces our spending power, especially over the long term. It means money today buys you more than the same amount of money next year. Here’s how inflation can affect the future value of £100 today at different rates.

| Annual inflation | Real value today | Real value of £100 in a year’s time | Real value of £100 in two years’ time |

|---|---|---|---|

| 2% | £100.00 | £98.00 | £96.04 |

| 5% | £100.00 | £95.00 | £90.25 |

| 10% | £100.00 | £90.00 | £81.00 |

By investing, your money could grow at a rate that outpaces inflation, helping you maintain and increase your wealth.

If your investment grows by 5% and inflation is at 2%, you’ve made a net gain of 3%. Importantly, it means you’ve made a real return – the value of your money has outpaced inflation and is now worth more.

The opposite is also true if your investment grows by less than the rate of inflation.

Investing in the stock market generally yields better returns than cash over the long term.

But it’s important to keep some cash tucked aside in a rainy-day savings pot for any unexpected emergencies. The amount depends on your circumstances.

| Pre-retirement | Retired |

|---|---|

| Three to six months' worth | One to three years' worth |

Any cash left over after covering the above, that won’t be needed for the next five years, could be invested.

Compounding

At a glance

Compounding should increase investment value over time. Imagine you invest a certain amount of money. Over time, this money earns returns. Now, instead of just taking out those returns, you reinvest them. This means your returns start earning returns too. This process is called compounding.

Compounding works best when you do nothing – just leave your money invested.

Consider regularly investing small amounts of money each month for your investments to gradually build up over time. It's good discipline - it takes the emotion out of your decisions, and you won’t be tempted to try timing the market. It’s also automatic, so once it’s set up the direct debit does the hard work for you.

What is compounding?

Compounding is where the earnings from your investment, like dividends, interest, or profit, are reinvested instead of being paid out – making returns on your returns. This should increase the overall value of your investment over time.

How to benefit from compounding

Compounding works best when you do nothing – just leave your money invested.

So as long as you’re diversified, and your investments are still in line with your goals, time will do the work.

Embedded-entry-block unknownType: textBlock

What is regular investing?

Another great way to grow your investments steadily over time is by investing monthly through direct debit.

Regularly investing small amounts of money, letting increases build up on themselves, and not touching it for the long-term takes patience – but the results could really pay off.

Why invest monthly?

Remove emotions and benefit from ‘pound-cost averaging’

The stock market always goes up and down, and you’ll want to buy when the price is low and sell when it’s high. But this is notoriously difficult to do well. Investing automatically gets you out of the mindset of trying to ‘time the market’ and spreads your money across different market conditions.

Sometimes, you’ll buy at a higher price, and other times it could be lower – but you won’t have to worry about the timing. Over time, these ups and downs tend to average out, called ‘pound-cost averaging’.

It’s good investing discipline

Setting aside money automatically makes it easier to get into good habits. You won’t forget to invest, because it happens at the same time every month. Any growth will compound on itself too. Leaving the money alone can be hard, and takes patience, but the results can really pay off over time.

Find out more about investing monthly by direct debit

All investments can fall as well as rise in value so you could make a loss. If you’re not sure if an investment is right for you, ask for advice.

Investment ideas for each account

If you’re not sure where to get started, our experts have chosen some investment ideas for our different accounts. But remember, it’s not personal advice. All investments can fall as well as rise in value, so you could get back less than you put in. If you’re not sure what to do, seek advice.