Plan for later life

The role pensions play in securing long-term financial resilience.

Important notes: This article isn’t personal advice. If you’re not sure whether an investment is right for you please seek advice. If you choose to invest the value of your investment will rise and fall, so you could get back less than you put in.

Pensions are meant for your retirement, so you normally can’t access your money until age 55 (57 from 2028), of which 25% is normally tax free and the rest taxed as income. Pension and tax rules can change, and benefits depend on your circumstances. Past performance isn’t a guide to the future. This article gives you information on how to make the most out of your pensions, but it isn’t personal advice. If you're not sure what's right for your situation, ask for financial advice.

Now we’ve covered your short-term financial resilience in the first three articles of the 5 to Thrive series, it’s time to start looking at your long-term resilience – pensions and retirement.

For most of us, pension savings will be our bread and butter when we stop working. However, we probably don’t always give them the TLC they deserve.

The good news is there’s a good chance you’re already doing some of the right things. Changes to pension rules back in 2012 have seen millions of us join and begin to contribute towards workplace pensions.

But lots of us still aren’t saving enough for retirement. Just two in five people are on course for a moderate level of income in retirement that's in line with the Pension and Lifetime Savings Association's (PLSA) income targets.

How much do I need for retirement?

Like most things, retirement is personal.

Everyone has different plans for their retirement years. Whether that’s where you want to live, what’s left on the bucket list or what you’d like to leave behind for your loved ones.

If you haven’t spent time thinking about these kinds of things, now could be a good time. Even if hanging up the old boots might seem like a country mile away, you can never be too prepared.

Understanding your retirement goals will help you to map out how much you’ll need to save each year. Once you’ve figured that out, you can then start to look at the level of risk you’re prepared to take with your investments to see if meeting your retirement goals is achievable.

Broadly speaking, more risk can equal more reward. Although more risk doesn’t always pay off so you could get back less than you invest.

For a ‘moderate’ retirement, the Pensions and Lifetime Savings Association estimates someone will need roughly £20,800 each year (£30,600 for couples).

If you want to live a more ‘comfortable’ retirement, it's estimated you’ll need about £33,600 each year (£49,700 for couples).

Less than half of people in the UK aged between 50-54, are on track to have a pension pot that will allow them a moderate retirement. For those over 60, it's less than 40%.

It's important to think about how any career breaks, or if you plan to retire earlier than the State Pension age, could affect how much you're able to contribute.

It’s worth pointing out, the amounts detailed above are based on people funding a lifestyle outside of London and the value of today’s money after tax.

If you’d like to find out more about how different age groups, income groups and regions are shaping up to receive a moderate retirement income across the UK, you can take a look using our Savings and Resilience Comparison Tool.

Reviewing your pension once a year to fine tune your retirement plans and check you’re on track is a good habit to get into. It also helps account for any changes to your circumstances.

You can check the estimated value of your pension pot and how much you might need to contribute each year with our pension calculator.

Bridging the gap

If the estimated value of your pension pot isn’t where you’d like it to be, don’t stress. You’re not alone. More than half of us worry about running out of money in retirement, according to Scottish Widows.

Boosting your pension savings is a lot easier than you might think – it involves time and using pension tax benefits to your advantage. Here are some approaches to help improve your retirement outlook.

Increase your contributions

All employers must now offer eligible employees a workplace pension and make contributions into it. Since 2019, the minimum contribution into your workplace pension is 8% of your pre-tax qualifying earnings. At least 3% of that comes from your employer.

We’ve already highlighted we need an estimated £20,800 a year for a moderate retirement. This could leave you more financially secure and give you some flexibility, compared to only having the minimum to get by through your retirement years. So it could be worth paying in that little bit extra if you can afford it.

Better still, your employer might even agree to match your contribution up to a set amount. If your employer does offer this, then don’t be shy, get as much free money as you can afford.

An extra few percent of your salary added each year might not seem like a big deal. But you’ll be surprised how quickly your pension pot could start to grow.

Cash in on tax relief

When you pay into your personal pension, and providing you’re a UK resident under 75, the government will boost eligible contributions with 20% tax relief which increases the overall amount added. If you pay tax at a higher rate you could claim up to an additional 25% (26% for Scottish Tax payers) in tax relief via your tax return.

Consider maximising how much you’re paying in. After all, opportunities to save tax, rather than pay it, are always welcomed.

There are limits on the value of tax-relievable contributions that can be added into a pension though.

Typically, you can add as much as you earn and receive tax relief each year. There is also an annual allowance (£40,000 for most people) which limits what you can pay in (including employer contributions and tax relief). Higher earners and those who’ve already accessed their pension might have a lower limit, or as a non-earner or someone with earnings of less than £3,600, up to £3,600 can be added each tax year.

Pension and tax rules can change, and benefits depend on your circumstances.

Work longer

Spending more time working doesn’t have to be a negative. If you find something you enjoy, you might be able to tailor your working hours to suit your retirement lifestyle. For lots of us, balancing part-time work in the early stages of retirement offers the best-of-both worlds.

However, it’s not always possible to work for longer. Illness, caring responsibilities and unemployment can get in the way of your gradual retirement plans, so it’s worth balancing any plans to work later with some of the other approaches.

Get your money to work harder

Workplace pension schemes start with a one-size-fits-all investment solution that you’re automatically invested into when you join the scheme. This is known as a default fund.

Default funds act as a useful starting block. For new investors, it’s a good way to dip your toe into the investing waters. It also avoids your pension savings being held as cash, which makes sense when looking longer term as the stock market has historically outperformed cash. Remember though, you cannot predict the future based on the past.

While default funds serve a purpose, they tend to be managed fairly conservatively. Taking control of where your pension is invested allows you to put your own personal spin on things while investing with your own risk criteria in mind.

That’s not to say first-time investors should abandon the default fund completely. You can consider starting off by adding other investments alongside your default for more diversification. As you learn more about investing and your confidence grows, you can continue to tailor your investment portfolio to suit you.

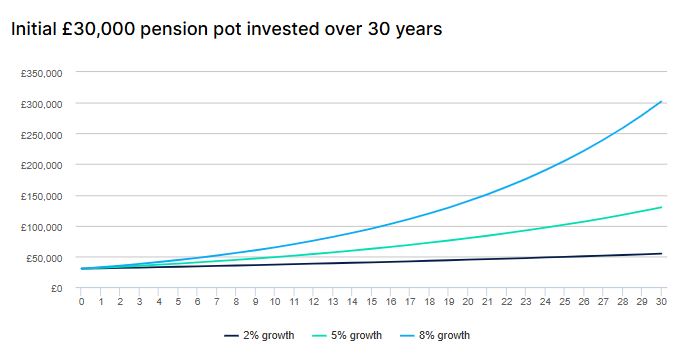

The graph shows how a change in investment performance can make a real difference to the size of the pot.

Illustration is based on a £30,000 initial investment with no further pension contributions. Actual performance would depend on the investments chosen. Figures exclude any charges which may occur. We haven’t factored in inflation.

The recipe for investing success is less complicated than some investors make out. Less is more when it comes to investing in the stock market – let time in the market and compounding do the hard work for you.

Remember, although investing over the long term improves your chances of investing success, nothing’s guaranteed. All investments can fall as well as rise in value, so you could get back less than you invest.

Need more help?

Deciding what’s best for your pension pot can be tricky. But the good news is, there’s lots of free guidance available should you need it.

MoneyHelper is a free and impartial government service for all things pensions related – from auto enrolment to the State Pension. You can learn about different topics by either taking a look at their useful online guides or speaking to their trained staff who can talk you through your options and key decisions

Pension Wise (run by MoneyHelper) is designed for people aged 50 or over. By speaking to one of their specialists, they’ll help you understand what type of pension you have, how you can access your savings and the potential tax implications of each option.

Read the rest of our 5 to Thrive articles

Control your debt

We look at why managing your debt is one of the five key building blocks for a financially secure future.

Protect you and your family

We take a look at why financial protection is one of the five key building blocks for a secure financial future.

Invest to make more of your money

We look at why investing is one of the five key building blocks towards a financially secure future.