Space Exploration Technologies Corp (SpaceX) has filed paperwork for a proposed Initial Public Offering (IPO), giving investors a detailed look at how the business is structured and how it makes money.

The filing shows a company built around three reporting segments – Space, Connectivity and artificial intelligence (AI). Space is the rocket business with Falcon, Dragon and Starship. Connectivity is mainly the orbital internet business, Starlink. And AI includes Grok, X and compute infrastructure.

So, we’re looking at each part of the business, the latest reported financials and the main risks disclosed in the IPO prospectus.

This article isn’t personal advice and should not be used in place of reading the IPO documents. Potential investors should always do their own research, read the full prospectus, and make their own investment decisions. Investments and any income from them will rise and fall in value, so you could get back less than you invest. If you’re not sure an investment is right for you, seek advice.

At a glance

SpaceX reported revenue of $18.7bn in 2025, up 33% on the year before. Growth in the most recent quarter slowed to 15% at $4.7bn. Revenue growth has come alongside ramping costs as the business invests in growth, putting pressure on margins and leaving profits in negative territory. Operating losses are rising, with the first quarter of 2026 already accounting for 75% of the total 2025 losses.

The three parts of SpaceX

SpaceX is split into three reporting segments, though they are linked in several ways.

Space

(22% of 2025 revenue)

Launch, rockets and Starship

Connectivity

(61% of 2025 revenue)

Starlink and satellite internet

AI

(17% of 2025 revenue)

Grok, X and compute infrastructure

Space – getting things into orbit

Space is the original SpaceX business – rockets, spacecraft and launches. It covers Falcon, the reusable rocket behind most of today’s missions, Dragon, the capsule used for cargo and crew, and Starship, the next-generation system designed for much larger payloads. Together, they form the side of SpaceX that sends satellites, cargo and people into orbit.

The financial picture is shaped by investment as much as revenue.

Space generated $4.1bn in revenue in 2025, but the segment was loss-making, with increased costs linked to Starship development. Starship is important because SpaceX connects it to several future areas, including next-generation satellites, satellite-to-mobile connectivity, and orbital AI compute (datacentres in space).

Connectivity – Starlink and satellite internet

Connectivity is mainly the Starlink business. It provides satellite-based internet and related services for households, businesses, governments and mobile users, using satellites in low-Earth orbit.

This is now the largest part of SpaceX by revenue. Starlink subscriber numbers have risen quickly, reaching 10.3mn in Q1 2026, while average revenue per user has come down over the same period. That gives two important facts at once – the customer base is expanding, and prices are coming down.

Connectivity is also the only profitable segment, unlike Space and AI, with $4.4bn of operating profit in 2025.

AI – Grok, X and compute infrastructure

AI brings together the language model Grok, the social media platform X (formerly Twitter), and AI datacentres. This part of SpaceX is about software, data and the physical computing power needed to train and run AI models. It’s also the newest of the three reporting units following the merger of SpaceX and xAI at the start of the year.

The segment is already generating revenue, but it’s also where the largest operating loss and the largest capital spending sit. AI accounted for the biggest share of group capital expenditure in 2025 (61%), and that accelerated into Q1 2026 (76%).

That spending is linked to the build-out of compute infrastructure, where it operates some of the largest AI compute clusters (datacentres) in the world. The aim is to use this to train its own models and rent out compute to third parties, like the recently announced Anthropic deal, which will bring in $1.25bn a month until May 2029.

Financial deep dive

SpaceX’s IPO filing gave plenty of financial detail. Here are some of the key details.

Profit

We gave a quick overview of profit above, where the data shows SpaceX is losing money for now – here, we’ll go one step further. SpaceX reports traditional measures like operating profit, net income, and earnings per share. But they also give adjusted EBITDA numbers.

We would caution, positive adjusted EBITDA is not the same as the company being profitable, it excludes some very real costs. But it helps investors get a view of the underlying business before major investment and financing costs.

Group adjusted EBITDA rose 23% in 2025 but fell 35% in Q1 2026. The Connectivity (Starlink) business is the main driver of performance, up 86% in 2025 and 29% in Q1 2026.

Capital Expenditure (Capex)

Capex is one of the clearest signs of where SpaceX is putting money to work.

Most of that spending is now tied to AI, which accounted for the biggest share of group capex in FY25 and again in Q1 2026, reflecting the build-out of compute infrastructure. Space and Connectivity also require ongoing investment, but the current capex profile shows how much of the near-term spending is being directed towards scaling the AI segment.

Cash Flow

Free cash flow gives a simple view of how much cash is left after running the business and investing in it. SpaceX is generating cash from its operations, but the level of capital spending means that free cash flow has been negative in recent periods.

Cash

SpaceX had $15.9bn of cash and equivalents at the end of Q1 2026.

The cash flow statement shows SpaceX has continued to raise external funding alongside cash generated from operations. It reported $26.4bn of cash from financing activities in 2025, which can include issuing new shares or debt.

On completion of the IPO, the cash balance would likely be significantly strengthened. However, $20bn of the debt position is a short-term bridge loan that must be paid down within 6 months of a successful IPO.

Segment Key Performance Indicators (KPIs)

Space

The Space data shows a launch business that’s been scaling in activity. Launches increased from 98 in 2023 to 170 in 2025, while mass to orbit rose from 1,210 metric tons to 2,213 metric tons over the same period.

That means SpaceX is sending more missions into orbit and carrying more payload with them, which is useful context for understanding the role this segment plays across launch customers, Starlink deployment and future projects tied to Starship.

Connectivity

Starlink is growing its customer base quickly, while average revenue per user has moved lower. Starlink subscribers rose from 2.3mn to 8.9mn from 2023-25, then reached 10.3mn in Q1 2026. Average revenue per user (ARPU) fell from $99 per month in 2023 to $81 in 2025, and then to $66 in Q1 2026.

Put simply, the service is expanding and reaching more customers, but the average monthly revenue from each subscriber has come down.

AI

The key AI performance measure focuses on how much computing power SpaceX is building. It’s not winning any prizes for having a simple name, but “nameplate compute draw” is essentially the maximum amount of power its data centres can use to run AI models.

That figure has increased from 0.3GW in 2024 to 0.8GW in 2025, reaching 1.0GW in Q1 2026. In simple terms, SpaceX is rapidly scaling the hardware behind its AI business, with more compute allowing it to train and run larger, more complex models, and rent spare capacity to third parties.

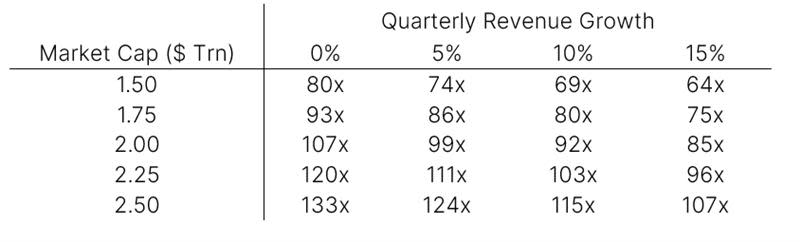

Valuation

Using the financial details held within the IPO document, investors can run a valuation analysis. Here, we’ve created a simple matrix to compare potential market caps against current and potential revenue run rates.

It's important to note that these market cap assumptions should not be taken as a prediction – they’re purely for illustrative purposes.

Forward Price to Sales Ratio:

Key Risks

SpaceX highlights several key risks in its IPO prospectus. The list below is not exhaustive – potential investors should read the full document.

Starship is central to several future plans, including next-generation satellites, satellite-to-mobile services and orbital AI compute. Delays or technical issues could therefore affect more than just the launch business.

Regulation is another key area. SpaceX needs approvals for launches, satellite services, and spectrum use, while the AI business introduces new risks around regulation, data, litigation, and access to high-demand chips.

Funding also matters. SpaceX has heavy investment plans, with no guarantee this will drive a return, so it may need to raise more external capital, which could add debt or dilute shareholders.

Public investors should also be aware of the dual class share structure. That means voting control is expected to remain concentrated with insiders, even after the IPO.