Calculating the yield

Important information: this section of our website aims to help you understand and use this important asset class. It is not personal advice. Neither income nor capital is guaranteed. The value of investments can fall as well as rise and you could get back less than you invest. Tax rules can change, and the benefits depend on your personal circumstances. Bonds may not be suitable for all investors. If you are unsure of their suitability for your circumstances, please ask for financial advice.

Investors will generally buy a bond for two reasons. The first is to lock in a known future income stream. The second is to attempt to benefit from rising bond prices. But what would cause the value of a bond to rise?

As with all traded assets, it will be down to supply and demand. There are two main variables affecting the price of bonds, the first being interest rates and the second the perceived credit quality or risk of default for the bond. As interest rates fall, a bond paying a fixed rate of interest every year will become increasingly sought after by investors.

Conversely, rising interest rates, perhaps accompanied by inflation, will make the fixed income stream unattractive to investors and the market price will fall. This relationship between price and yield is the key to understanding the factors moving the fixed income markets.

Price and yield

To understand the return on fixed income instruments is to view a bond as a series of discounted cashflows. At the start of the period, the investor pays out cash to purchase the bond. Over the course of the bond's life, the investor should then receive several payments, usually one or two a year from interest payments and a final repayment at the end of the bond's lifespan. In this respect, bonds differ fundamentally from equities, where the future cashflows are unknown.

Given that future cashflows are known quantities, the relationship between the price of a bond and its yield is governed by mathematical formulae. We are going to look at three methods of analysing a bond's yield: the income yield, the simple yield, and the yield to maturity (YTM).

Income yield

Imagine a bond with a 5% coupon (divided into two semi-annual payments) maturing in exactly one year's time. If you bought the bond at the face value of 100p or "par", we know we would receive an income 5% per annum on our investment until maturity.

But what if you paid less than par for the bond? Assume that we purchase the same bond for 95p. Our income (or "running") yield would be:

Par/purchase price * coupon = running yield

Or 100/95 * 5% = 5.26% per annum.

Buying a bond above par has the effect of reducing the bond's income yield. If you bought the bond above for 112p, the income yield would drop to 4.46%.

100/112 * 5 = 4.46% per annum

The income or running yield (sometimes also known as the flat yield) does not take into account any profit or loss made by holding the bond to redemption and simply assumes that the investor will be able to sell the bond at the same price they purchased it for. For a more accurate measure of yield, we must turn to the yield to maturity, the standard calculation employed by market professionals, also known as the redemption yield.

Before we turn to the more complex (and more accurate) yield to maturity, it is worth considering the "simple yield". This is a good rough guide to the return available on a bond and can often be worked out in one's head.

Why does the price of some bonds move more than others?

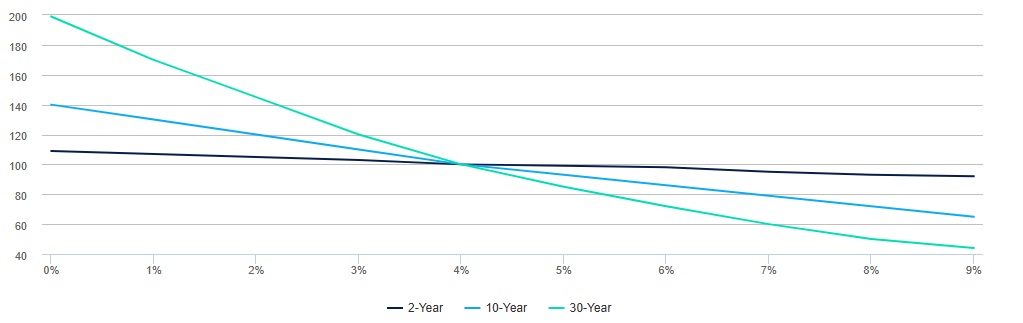

The price of some bonds will move more than others because of a variety of factors, including the bond's duration. Duration is a measure of the sensitivity of the price of a bond or other debt instrument to a change in interest rates.

As a bond’s duration rises, its interest rate risk also rises because the impact of a change in the interest rate environment is larger than it would be for a bond with a smaller duration. For example, if rates were to rise 1%, a bond with a five-year average duration would likely lose approximately 5% of its value.

If rates are expected to increase, consider bonds with shorter durations. These bonds will be less sensitive to a rise in yields and will fall in price less than bonds with higher durations.

If rates are expected to decline, consider bonds with higher durations. As yields decline and bond prices move up, higher duration bonds stand to gain more than their lower duration counterparts.

The below graph is an example of the correlation between yield and price changes on bonds with the same coupon but differing durations.

This is a hypothetical example for illustrative purposes only. It is not intended to reflect the actual performance of any bond.

The yield curve

Both government and corporate bonds are issued in a variety of maturities, ranging from super-short 3-month treasury bills and corporate paper through to 30-year or even undated or “perpetual” bonds with no final maturity.

Interest rates change over time, and bonds of different maturities will have different yields, reflecting the market's expectations for future interest rates. Generally, investors will require an incrementally higher yield for longer dated securities. This means that long-dated bonds generally yield more than short-dated bonds. This is known as a “positive yield curve” and is the usual state of play in the markets. If investors expect interest rates to rise in the future, the price of longer dated bonds will fall, pushing up yields at the long end of the curve. This is known as a “steepening” of the yield curve.

Alternatively, the perception of falling interest rates can lead to an “inverse” yield curve, where investors scramble to lock in fixed rates at the long end, pushing yields down below current money market rates.