It’s one of the most natural instincts in investing – to look at what’s performed well and assume it will keep doing so.

But looking back over the past 20 years, it’s not always straightforward. Sectors or regions that deliver standout performances in one year often are not leaders of the pack 12 months later. Similarly, areas that have disappointed can recover sharply, sometimes when investors least expect it.

This article is for information only and not personal financial advice. Investing can help your money grow, but the value of investments can rise and fall, so you could get back less than you put in. Investing is for the long term, typically 5 years or more.

If you’re not sure investing is right for you, a financial adviser can help.

Leadership does not stand still

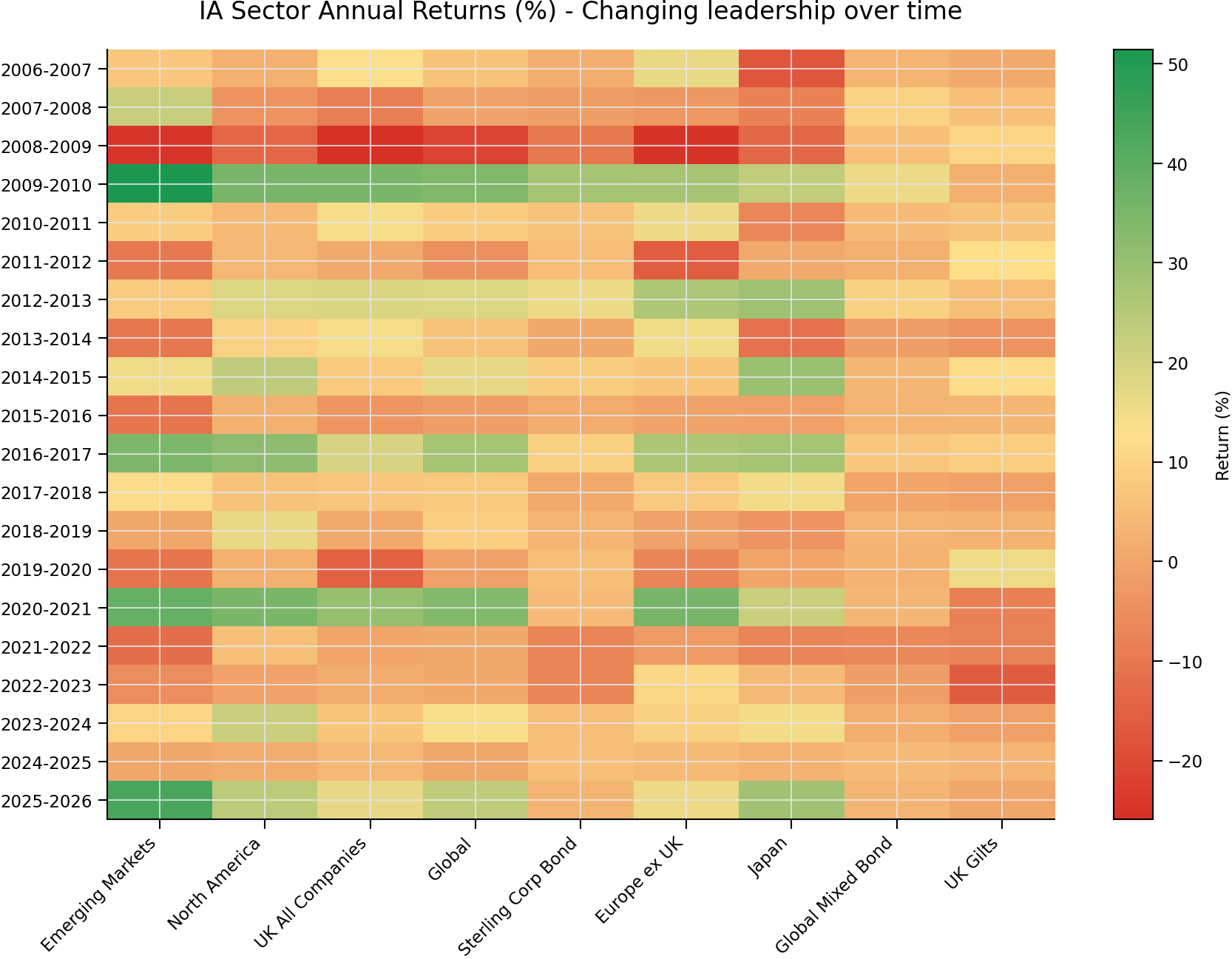

Leadership across the major Investment Association (IA) sectors has shifted regularly from one year to the next. Emerging markets, for example, have produced table topping returns in some years, with gains of more than 50% in 2009/10 and in the region of 40% in others. Yet it’s tended not to be one of the strongest performers the following year and has seen losses on some occasions.

Japan shows a similar pattern. Strong rallies, with returns exceeding 20% over several one-year periods, only to be followed by periods of weaker performance and occasional declines. We see similar trends in major regions like Europe and the UK.

What’s clear is that no single region or sector consistently outperforms. Leadership rotates, sometimes gradually and sometimes abruptly. A market that’s leading one year can easily fall behind the next.

This matters because many investors make decisions based on recent performance. When a particular region has delivered strong returns, it’s easy to feel confident investing more. But by the time those returns are widely recognised, much of the upside may have already been realised.

The chart below represents the annual returns for several major IA sectors, to the end of April each year.

Past performance isn’t a guide to future returns. Source: Lipper IM to 30/04/2026

Even long-term winners have setbacks

The US – the IA North America sector – stands out as one of the stronger performers over the period, particularly in the past decade. In recent years it’s been the strongest performer more than once, reflecting the strength of large US companies and the growth of sectors like technology.

But even here there are years of weaker performance where returns have been relatively modest compared to other regions.

For investors with a lot invested in a single region, this could be a risk. Strong long-term trends can persist, but they don’t move in a straight line.

The UK provides a different perspective. Over the last 20 years, the IA UK All Companies sector hasn’t performed as well, but it’s been the second-best performing sector on several occasions. It also provides important diversification, as more of the UK market is focused on sectors like financials and energy.

What about bonds?

It’s not just stock markets where patterns can change. Bonds are traditionally seen as steadier and more defensive – this means they don’t tend to demonstrate extreme market moves in the same way company shares might do. That said, they still experience both good and bad periods.

Corporate bonds and gilts (UK government bonds) have generally delivered lower but more stable returns over the long term and can hold up better when stock markets fall. There have even been years – like in 2024/25 - when corporate and mixed bonds sat at the top of the performance table.

Perhaps most memorably, UK gilts and global bonds (as measured by the IA Global Mixed Bond sector) delivered a positive return during the fallout of the 2008 global financial crisis, whereas equity markets suffered steep losses.

But there are also years when bonds have lost money. Bonds fell around 2021-23 when interest rates were rising – because yields (a measure of the income bonds pay) look less attractive when the interest on cash starts to look more appealing.

This doesn’t mean bonds no longer have a role to play, but their behaviour can change depending on the environment. Recently, higher inflation expectations have led to rising bond yields, and this could offer investors an interesting opportunity to take a closer look at this asset.

The behavioural trap

Despite the best-performing sector changing from year-to-year, there’s still a temptation to chase performance. Similarly, long periods of poor performance can see people selling other areas just as their prospects begin to improve.

However, by the time a trend becomes obvious, share or bond prices often already reflect much of the good news. This leaves less room for further growth and creates potential for disappointment.

Equally, weaker areas are not always destined to stay that way. Some of the strongest returns in the data follow periods of poor performance, as sentiment shifts and conditions improve.

All this doesn’t mean investors should simply buy the worst-performing sectors in the hope of a rebound. Underperformance can reflect genuine issues, and recovery can take time.

Stay focused on the bigger picture

Over the past 20 years, markets have moved through very different environments, from the global financial crisis to periods of low interest rates and, more recently, rising inflation and higher rates. Throughout all of this, leadership has shifted.

Trying to work out when those shifts will happen is extremely difficult. What investors can control is how they position themselves to deal with that uncertainty.

Investing across regions and asset classes helps reduce reliance on any single area and allows investors to benefit from different sources of return over time. It also helps manage the emotional side of investing. A diversified portfolio is less likely to be dominated by the extremes of any one market, making it easier to stay invested through changing conditions.

The Wealth Shortlist could be a great starting point for investors looking to build or diversify their portfolio. It features what our expert Research Team believes to be funds with great long-term performance potential across a range of sectors.

30/04/2021 To 30/04/2022 | 30/04/2022 To 30/04/2023 | 30/04/2023 To 30/04/2024 | 30/04/2024 To 30/04/2025 | 30/04/2025 To 30/04/2026 | |

|---|---|---|---|---|---|

IA UK All Companies | -0.13 | 1.62 | 6.80 | 4.06 | 16.39 |

IA North America | 5.96 | -0.56 | 21.69 | 1.57 | 23.91 |

IA Sterling Corporate Bond | -7.37 | -6.89 | 5.41 | 6.02 | 3.40 |

IA UK Gilts | -7.71 | -16.09 | -1.11 | 3.40 | 0.12 |

IA Global | 0.51 | 0.58 | 13.87 | 0.26 | 23.17 |

IA Global Emerging Markets | -12.22 | -5.13 | 10.20 | 0.14 | 43.28 |

IA Europe Excluding UK | -2.54 | 10.71 | 9.29 | 4.34 | 15.65 |

IA Japan | -7.07 | 4.80 | 14.81 | 2.87 | 28.26 |

IA Global Mixed Bond | -6.36 | -1.33 | 2.13 | 4.92 | 3.41 |