Software and data analytics stocks have taken a sharp hit in recent months, and artificial intelligence (AI) anxiety is right at the centre of it. Investors are increasingly worried that powerful new models could make parts of today’s software stack cheaper, easier to replicate, or even redundant. That fear has been enough to trigger a broad selloff, sweeping up winners and laggards alike.

But when markets move this fast, nuance often gets lost.

AI will undoubtedly reshape the industry, yet not every software business faces the same level of risk – or opportunity. For investors willing to slow down and look at fundamentals, this pullback might say more about short-term sentiment than long-term value.

We’re looking at what’s happened, why investors are concerned, and where we think the opportunities are.

This article isn’t personal advice. If you’re not sure an investment is right for you, seek advice. Investments and any income from them will rise and fall in value, so you could get back less than you invest. Ratios also shouldn’t be looked at on their own. Past performance is not a guide to the future.

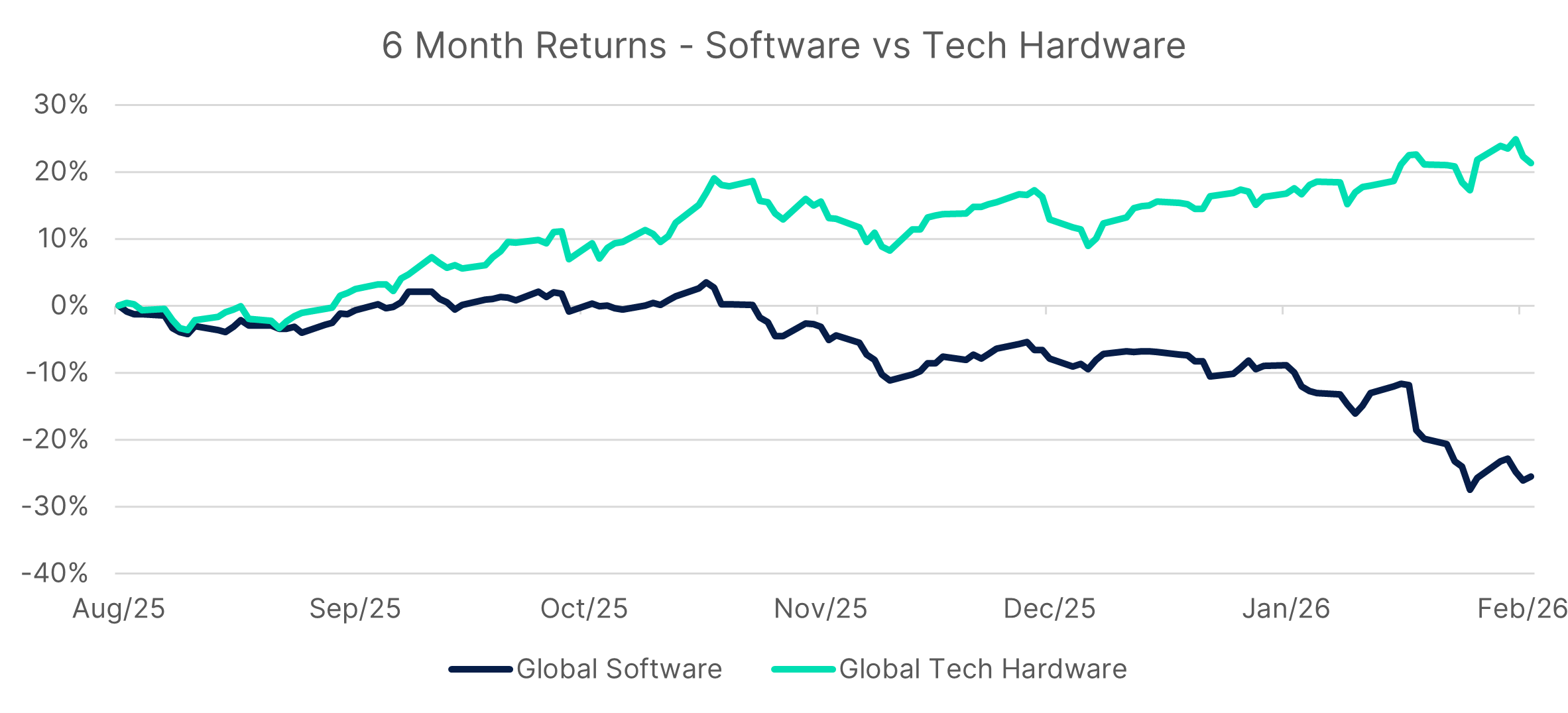

The tech sell-off

The scale of the move has been striking.

On forward multiples, US-listed software is now trading at a discount to the broader market – something that’s only happened once before in the last 30 years. That alone tells you this isn’t a routine pullback, but a meaningful reset in how investors are pricing risk.

Crucially, this hasn’t been driven by a wave of earnings downgrades or collapsing near‑term demand. In fact, recent results have been strong, but the market is looking further ahead. The concern is less about disruption today and more about what software economics might look like two, three, or four years out as AI capabilities accelerate.

Recent advances from private AI players have brought that future forward in investors’ minds. New tools from companies like Anthropic have raised questions about how defensible analytics and workflow software really are, especially given the fast pace of innovation.

In other words, this has been a broad repricing of uncertainty about the future, not a verdict on the present.

Software to hardware

Looking at the bigger picture, this isn’t a market-wide shift to seemingly safer investments. Equity markets are still trading near all-time highs, which tells us investors haven’t pulled money out of stocks completely – they’ve simply moved it around. This has been a sector-specific rotation, not a loss of confidence in equities.

A big chunk of that capital has flowed into AI hardware and infrastructure.

Many chipmakers, energy providers, and construction names have benefited as investors position for a world that needs more physical investment for powering AI.

And this makes sense with our view that AI economics will likely favour hardware more than during the software-dominated internet era.

Running AI systems is inherently compute-intensive and involves recurring software deployment not just one-and-done installations. Models need to be trained, retrained, and run at scale, driving persistent demand for chips, power, and physical infrastructure. This dynamic just isn’t being talked about enough, but over time it matters – a larger share of industry profits might accrue to hardware, creating a structural headwind for parts of the software sector.

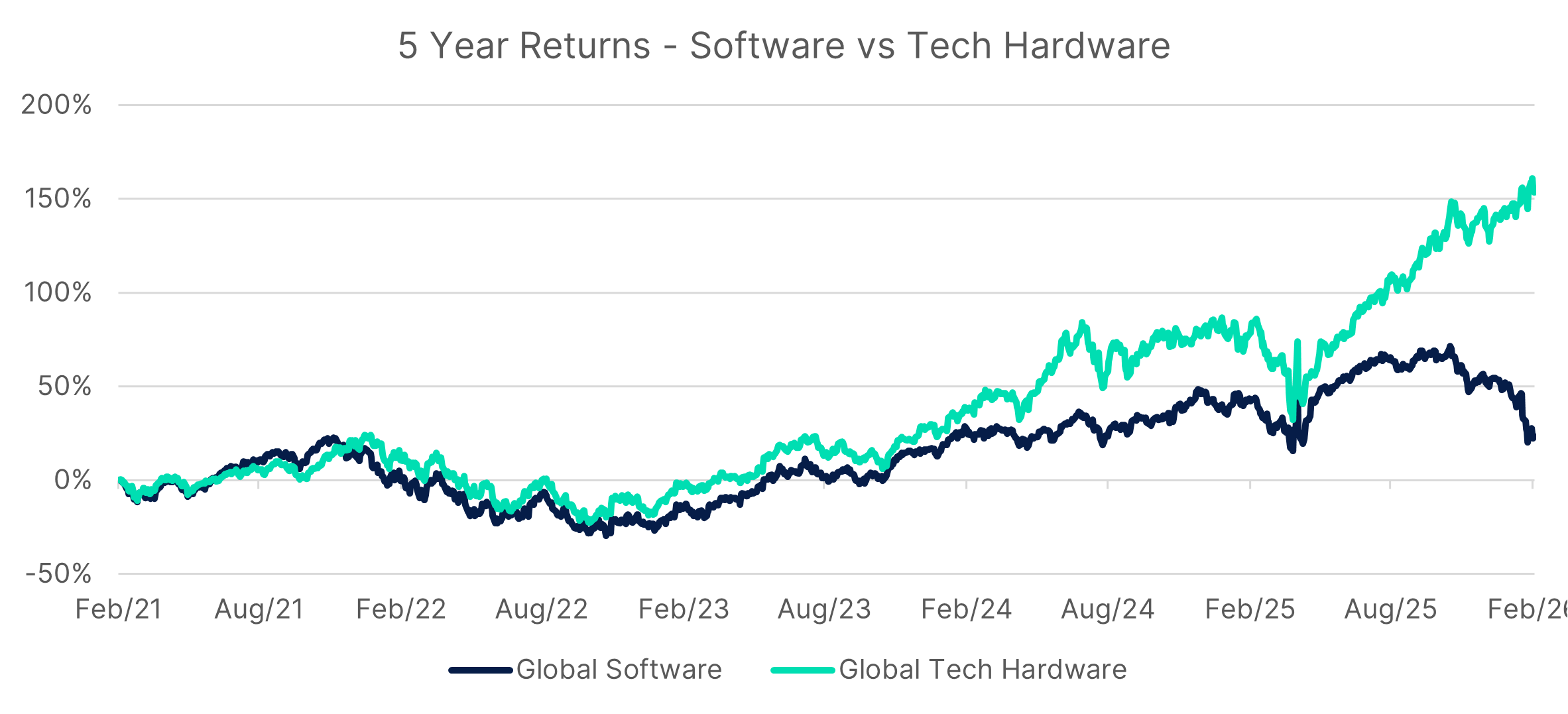

If we zoom out from the previous graph and look instead over 5 years, we can see that this has already been playing out behind the scenes – only at a slower pace.

The AI hardware opportunity

So where do we go from here?

We believe the risks around AI are real, and the premium valuations that software names have sat on for years are rightly in question. And we think software companies are likely to share more of the economic upside with hardware providers than they did in previous technology cycles.

Even so, the speed and indiscriminate nature of the sell-off looks overdone to us. We see this reset creating an opportunity to invest in high-quality names at more attractive valuations.

So, here are the key areas we’re focusing on to identifying potential AI winners in the software/data space.

Proprietary data – AI tools might lower barriers at the application layer, but they don’t magically recreate years of high-quality, proprietary data.

Software businesses sitting on unique datasets, deeply embedded in customer workflows, have a strong advantage because those datasets are hard to replicate, expensive to curate, and improve with scale. In many cases, the data is the product, and AI simply becomes a new way to extract more value from it rather than a substitute.

Switching costs – the deeper the software is embedded in a customer’s operations, the harder it is to replace. Ripping out a core system isn’t like swapping a productivity tool - it’s more like open-heart surgery, with operational risk, downtime, retraining, and often regulatory or contractual complexity.

High switching costs don’t eliminate disruption risk, but they do slow it materially and give incumbents time to adapt.

Regulated industries – regulated sectors remain among the most defensible areas of software and data in our view. Vendors here have spent years building trust not just with customers, but with regulators, auditors, and compliance teams.

In industries where mistakes are costly and scrutiny is high, buyers are far less willing to experiment, making disruption slower and more selective - and in our view, creating a more resilient long-term opportunity for established providers.

Two Investment Ideas

Investing in an individual company isn’t right for everyone because if that company fails, you could lose your whole investment. If you cannot afford this, investing in a single company might not be right for you. You should make sure you understand the companies you’re investing in and their specific risks. You should also make sure any shares you own are part of a diversified portfolio.

RELX

RELX has continued to show its quality, delivering a characteristically strong set of 2025 full-year results.

We were encouraged by the positive commentary on the AI rollout, even as the market continues to question its ability to defend against AI disruption. Importantly, AI is being layered onto an existing data‑driven franchise that’s already deeply embedded in regulated end‑markets.

The investment case rests on RELX’s deep, proprietary datasets and mission‑critical analytics used by insurers, law firms, and academic institutions – areas where trust and accuracy really matter. Fully digital products now account for 84% of group revenue, with over half recurring, creating high switching costs and resilient cash flows.

With improving shareholder returns, a strengthening balance sheet, and AI still in the early innings, we think recent weakness looks overdone and RELX features on our 5 Shares to Watch list for 2026.

That said, we don’t think sentiment will shift overnight, and some disruption fears are valid. Investors will need plenty of patience, and RELX is under more pressure than ever to keep delivering.

Nvidia

For investors thinking software is just too hard to call, Nvidia is still our preferred AI hardware name.

A key reason it’s featured on the 5 Shares to Watch list two years in a row is our conviction that AI will keep directing a larger share of value toward the hardware layer. As running AI systems becomes increasingly resource‑intensive, Nvidia sits at the centre of that value transfer.

Concerns around custom chips and alternative suppliers haven’t gone away, but we think they’re often overstated. Designing a chip that looks good on paper is one thing, delivering performance, reliability, and scale in real‑world deployments is another. And that’s where Nvidia’s track record stands apart.

Its breadth is also underappreciated. It’s a fully integrated data centre stack spanning chips, software, networking, and system design, with rapid product cycles delivering meaningful gains in both performance and energy efficiency.

In our view, Nvidia is best in class and one of the cleanest ways to gain exposure to AI demand at the hardware layer.

But there are risks. Like a slowdown in the AI buildout or the ability to supply rapidly rising demand.

The author holds shares in RELX and Nvidia.

This article is original Hargreaves Lansdown content, published by Hargreaves Lansdown. It was correct as at the date of publication, and our views may have changed since then. Unless otherwise stated estimates, including prospective yields, are a consensus of analyst forecasts provided by LSEG. These estimates are not a reliable indicator of future performance. Past performance is not a guide to the future. Investments rise and fall in value so investors could make a loss. Yields are variable and not guaranteed.

This article is not advice or a recommendation to buy, sell or hold any investment. No view is given on the present or future value or price of any investment, and investors should form their own view on any proposed investment.