The start of a new tax year is a great time to review your portfolio and make the most of your allowances. Adding and investing new cash early can help maximise your returns.

ISAs and pensions are a powerful long-term tool, shielding investments from income tax and capital gains tax, which makes them well suited to building wealth over time.

None of our picks this year are designed to be standalone solutions, but as part of a broader, diversified portfolio aligned to your objectives and attitude to risk. You could invest in one, two or all three.

This article isn’t personal advice. If you’re not sure an investment is right for you, seek advice. Investments and any income from them will rise and fall in value, so you could get back less than you invest. Past performance is not a guide to the future. Ratios also shouldn’t be looked at on their own.

Investing in an individual company isn’t right for everyone because if that company fails, you could lose your whole investment. If you cannot afford this, investing in a single company might not be right for you.

You should make sure you understand the companies you’re investing in and their specific risks. You should also make sure any shares you own are part of a diversified portfolio. It’s important to check in on your portfolio from time to time to make sure your investments are still in line with your goals. ISA, pension and tax rules change and benefits depend on personal circumstances. Money in a pension is not usually accessible until age 55 (57 from 2028).

ISA share ideas

ISA share ideas

Mastercard

Mastercard is best known for running one of the world’s largest payment card networks. Card payments have been at the forefront of multiple shifts in payment technology, from the demise of cheques, through to online shopping and contactless payments, and increasingly integration with digital wallets. That’s underpinned a long and resilient track record of growth. The continuing increase in card usage is supportive of more to come.

But that’s not the only string to Mastercard’s bow. It sells a range of value-added services, including cybersecurity and data analytics, to its customer base of financial institutions and retailers. Mastercard’s leadership on this is driving margins higher, and we see further growth ahead for services. This, along with the company’s exposure to regions with higher structural growth potential, are among the reasons it’s our preferred name in the space.

It sells a range of value-added services, including cybersecurity and data analytics, to its customer base of financial institutions and retailers.

However, the fast-changing nature of the payments industry also provides challenges to Mastercard’s ecosystem. The company’s on the front foot with this, embracing rather than resisting change, but disruptive technology is a threat we’re monitoring closely.

There’s also political pressure on prices charged both by credit card issuers and payment processors, which has put the valuation under pressure.

Marks & Spencer

Marks & Spencer’s shares have rallied since we selected it as one of HL’s Five Shares to Watch in 2026. Nonetheless, our investment case still stands as it seeks to rebuild after a cyberattack hamstrung performance, driving a sharp decline in first-half profits.

Operations are expected to return to full flow by the end of March, sparking hopes that second-half profits can rebound above last year’s level. Looking further ahead, the cyber-incident looks to have sharpened management’s focus on operational and strategic improvements, and we’re optimistic that the group can bounce back stronger.

We think the worst is behind Marks & Spencer now. Sitting at a discount to peers, the valuation still offers attractive upside in our view.

Performance in the Food division remains positive, with sales growing ahead of the broader market thanks to impressive volume growth. Recent industry data also suggests the group is continuing to gain market share. M&S’s store rollout programme should help on this front too, aiming to grow its presence in under-served areas of the country.

The Fashion, Home & Beauty division is where we see the biggest long-term opportunity. The online journey and margins simply aren’t as good as the competition. Big investments are being made to fix this, and if successful, could deliver a strong uplift in profitability.

We think the worst is behind Marks & Spencer now. Sitting at a discount to peers, the valuation still offers attractive upside in our view. But competition is fierce, and M&S needs to nail its execution to deliver the expected improvements.

SIPP share ideas

SIPP share ideas

Intuitive Surgical

Intuitive Surgical is the dominant name in the complex field of robotic surgery, a space where we see the potential for a long runway of growth. These incredibly precise systems improve surgical outcomes and recovery periods, which also provides an economic benefit for healthcare providers.

The company finished 2025 with good momentum. However, this year’s guidance for 13-15% growth in the number of operations carried out using the flagship da Vinci platform was a fair clip below last year’s pace of 18%. There are some headwinds to be mindful of, including competition in China and slowing demand for certain procedures due to the success of anti-obesity medicine. Management is known for being cautious, and although it’s never a given, we think guidance may improve as the year progresses.

Intuitive Surgery’s lofty valuation reflects its leading position in an attractive market.

A full roll-out of the company’s most advanced platform presents an opportunity to upgrade existing users and win new customers, in a large market where penetration remains low. New use cases such as heart surgery are further expanding the prize on offer.

Intuitive Surgery’s lofty valuation reflects its leading position in an attractive market. Nonetheless, we still think there’s room for meaningful upside from here given the growth prospects. But with no major catalyst since being highlighted as one of our Five Shares to Watch for 2026, sentiment has waned. Geopolitical uncertainty could also keep a lid on enthusiasm in the near term.

Meta

Meta remains one of the most compelling platforms in the digital ecosystem, sitting at the intersection of global social connectivity and advertising. Its family of apps, spanning Facebook and Instagram through to newer platforms like Threads, offers advertisers access to a vast and still‑growing audience, with AI increasingly improving how effectively those users can be reached and monetised.

Recent performance underlined the strength of that engine. Ad impressions rose 18%, pricing continued to firm, and revenue guidance landed at the top end of expectations – a familiar pattern. AI-driven tools are enhancing user engagement while delivering better returns for advertisers, allowing Meta to extract more value from its already enormous base.

Ad impressions rose 18%, pricing continued to firm, and revenue guidance landed at the top end of expectations – a familiar pattern.

The current valuation reflects the risks but gives little credit for potential rewards. We think that with strong execution and backing from substantial cash flows, the narrative can shift. However, execution risk on all that investment is real, particularly if revenue growth softens while costs continue to rise.

Income share ideas

Income share ideas

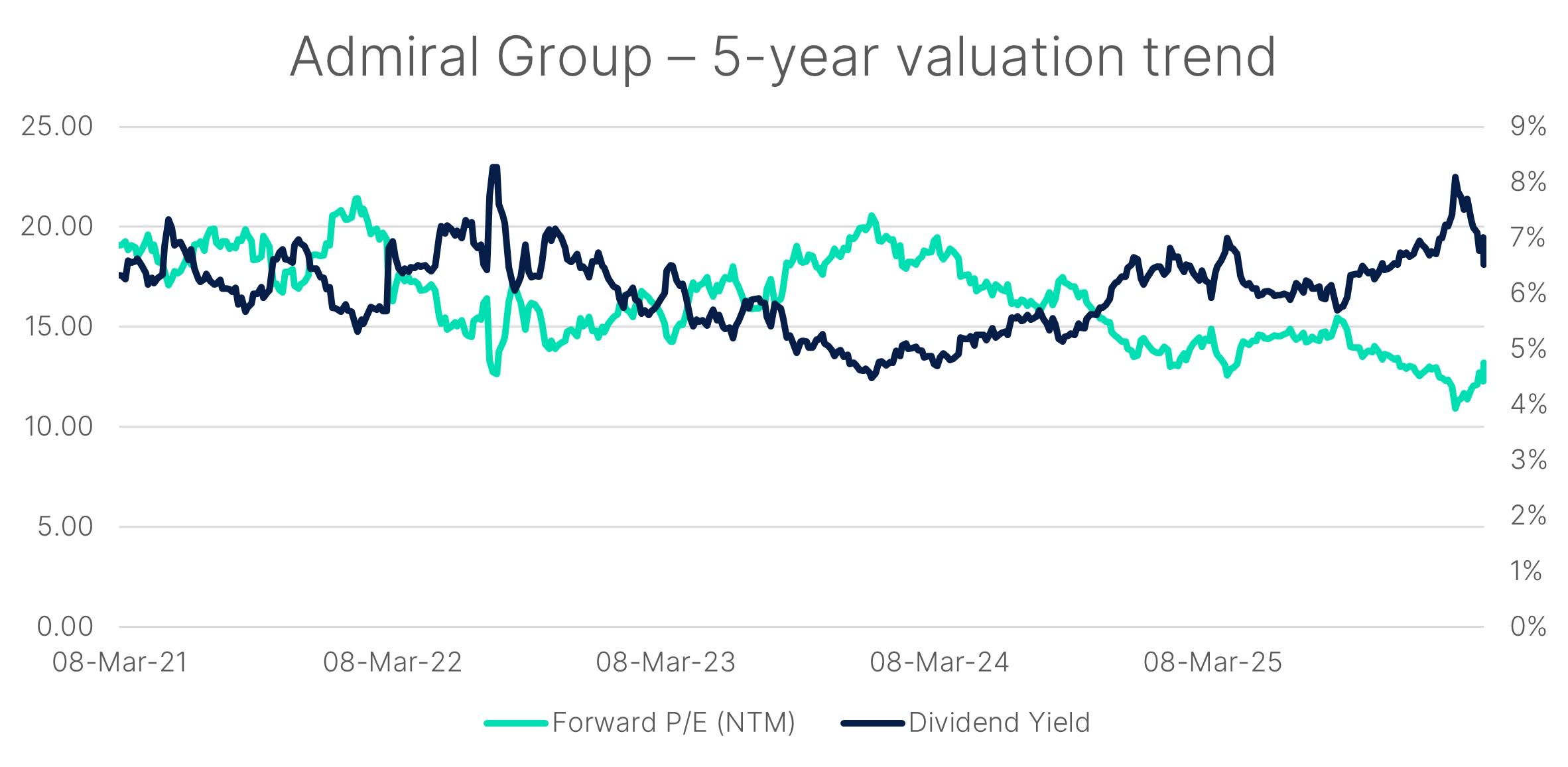

Admiral

Admiral’s shares have been volatile, but even so, we continue to view the group as a high-quality operator with a business model that sets it apart from many peers.

One of Admiral’s key advantages is its investment in data and technology, which helps it better understand risk and price policies more accurately, particularly in UK motor insurance.

Profits are expected to decline in 2026 as market conditions normalise, but we expect signs of improvement to emerge throughout the year, with the outlook for 2027 looking better.

Selling mainly direct to customers also gives the company access to more complete information, which can support better pricing decisions and more consistent profitability over time.

The group’s approach to growth is also relatively unique. Admiral works with reinsurance partners to share some of the risk on the policies it writes, allowing it to grow when market conditions are favourable without putting too much pressure on its balance sheet, helping to reduce earnings volatility.

Profits are expected to decline in 2026 as market conditions normalise, but we expect signs of improvement to emerge throughout the year, with the outlook for 2027 looking better. In our view, this has created an opportunity to gain exposure to a quality insurance business with an attractive dividend yield.

That said, no returns or income are guaranteed, and profits in UK motor insurance remain sensitive to claims inflation, competitive pricing and potential regulatory pressure.

RELX

We’ve liked RELX for some time, and with shares under pressure in recent months, we see this as an attractive entry point into a high-quality business. Concerns around whether established data and analytics groups could be disrupted by the rapid development of new AI tools have weighed on sentiment, but the company’s latest results continue to point to a business executing well.

RELX provides mission-critical data analytics to insurers, law firms and academic institutions. Its competitive advantage is built on deep, proprietary datasets and sophisticated tools that are difficult to replicate. Digital products remain the core driver of the group, accounting for the vast majority of revenue and the bulk of long-term growth.

Its competitive advantage is built on deep, proprietary datasets and sophisticated tools that are difficult to replicate.

AI fears aside, analytics remains a relatively defensive area, with a large proportion of revenues recurring through subscription models, providing good visibility and resilience across the cycle. Cash generation is strong, supporting ongoing investment alongside shareholder returns, including an increased pace of buybacks – though not guaranteed.

RELX is also featured on our Five Shares to Watch list for 2026 and, in our view, remains well-positioned to grow earnings over the long term. We see scope for sentiment to recover, but are conscious that this could be a slow process, and AI uncertainty is a very real risk.

One or more of the authors and/or connected parties hold shares in RELX.

One or more of the authors and/or connected parties hold shares in Meta.

This article is original Hargreaves Lansdown content, published by Hargreaves Lansdown. It was correct as at the date of publication, and our views may have changed since then. Unless otherwise stated estimates, including prospective yields, are a consensus of analyst forecasts provided by LSEG. These estimates are not a reliable indicator of future performance. Past performance is not a guide to the future. Investments rise and fall in value so investors could make a loss. Yields are variable and not guaranteed.

This article is not advice or a recommendation to buy, sell or hold any investment. No view is given on the present or future value or price of any investment, and investors should form their own view on any proposed investment.