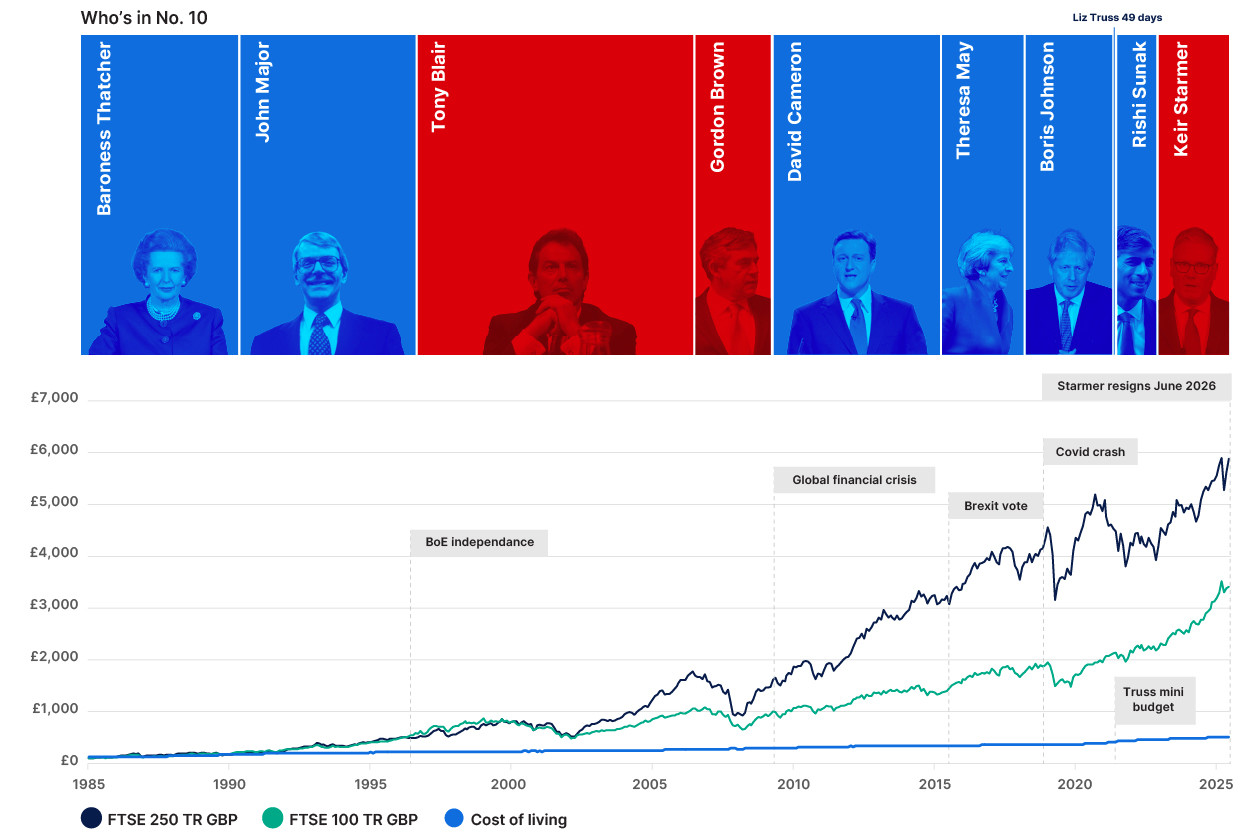

Since Hargreaves Lansdown was founded in 1981, we have had ten prime ministers, two serious inflation shocks, a financial crisis, referendums and a global pandemic. And the growth line may wobble, but it does not – over any sensible holding period – stop climbing.

How UK stock markets have grown over the long term

A hundred pounds left in the FTSE 250 at the end of 1985 is worth around £5,882* today. The same hundred in the FTSE 100 is worth roughly £3,409. The cost of living over the same span has risen to about £323, meaning prices more than tripled. Set those three lines on one chart and the most important investment lesson is simple – stay invested and let time do the heavy lifting. Although as always, remember that the past is not a reliable guide to the future.

The steeper of the two equity lines belongs to the FTSE 250, which is no surprise. The mid-cap index is more domestic and more home-grown than the FTSE 100, and its constituents are much smaller companies. Smaller companies have historically been seen as businesses still early enough in their lives to compound earnings quickly.

Over the long run, that has translated into a meaningful premium over the blue chips, with the mid-cap finishing some thirteen times ahead of inflation, against roughly seven times for the FTSE 100.

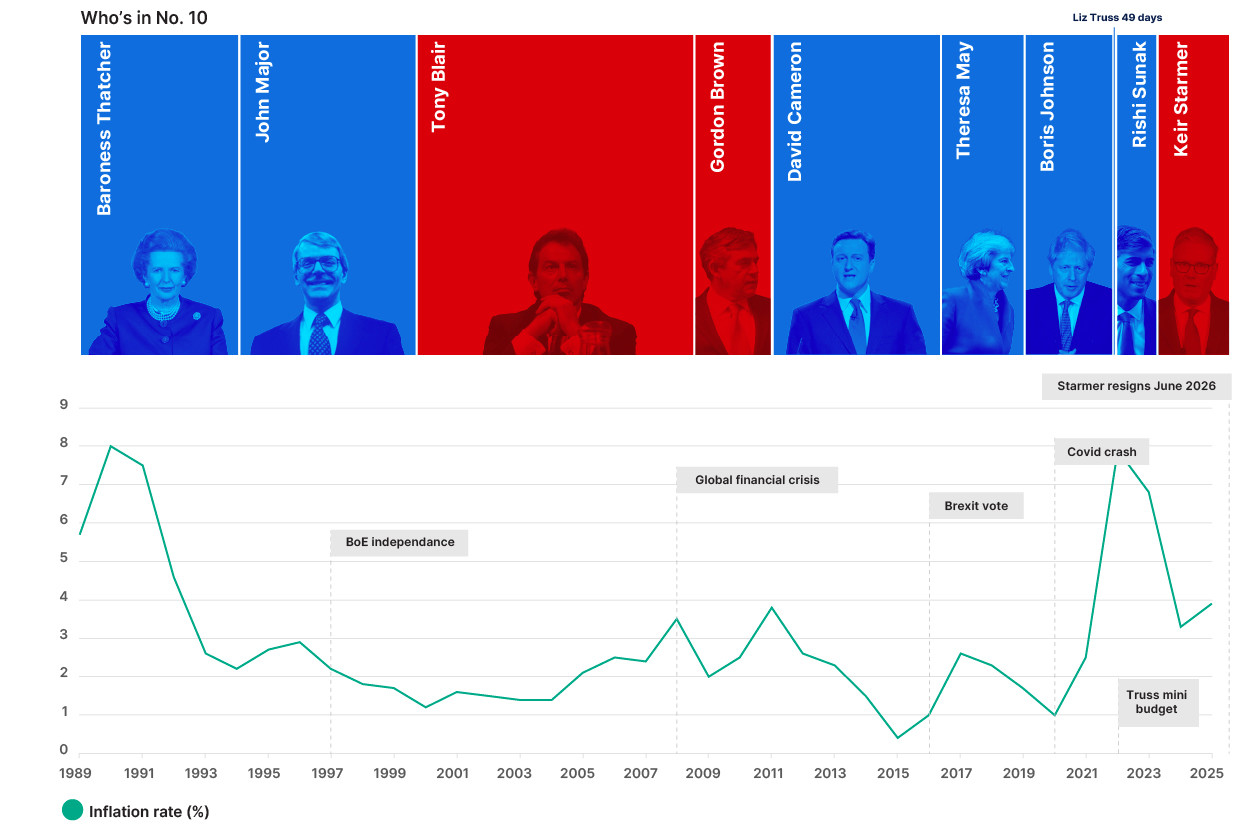

How inflation shapes markets and governments

It’s not just about market growth though, it’s also important to consider inflation. This matters because inflation is not just an economic number. It changes the political weather.

When inflation is low and stable, it is easier to govern.

Major, Blair, Brown and Cameron between them presided over an unusually benign run. The foundation for it was reinforced in 1997, when the incoming Labour government handed the Bank of England operational independence and set it a clear inflation target. That institutional decision gave investors, households and businesses a more transparent and credible regime. The rules were clearer and the referee was independent.

When inflation came back, through Covid, the energy shock from the war in Ukraine and higher interest rates, politics became more brutal.

High inflation does not merely raise the cost of the weekly shop. Over time, it creates a deeper feeling that things are not getting better. A country that no longer believes its children’s future will be better than its own is a difficult country to lead.

That helps explain why political change has felt so relentless. Britain is on course for its seventh leader in a decade. But for investors, the important point is that political instability and market returns are not the same thing. The chart contains plenty of political upheaval. It also contains decades of wealth creation.

There is a market lesson here too. Governments can shape the investment backdrop through tax, regulation, spending and confidence. But markets tend to judge outcomes rather than personalities. The events of 2022 showed how quickly confidence can be lost when policy looks unfunded or detached from economic reality. Credibility matters.

But credibility is not the same as political certainty. Investors do not need politics to be calm before investing. If they had waited for calm since 1985, they would have spent most of the last forty years waiting.

Why diversification and long-term investing matter

Companies that invest well for the long term can generate growth. Over time, that growth is what investors are trying to capture.

For investors, the questions worth asking are not really about the next reshuffle. They’re about whether the businesses you own can grow earnings, protect margins, adapt to change and compound value over time.

That is why diversification matters.

It is also why regular investing matters. A portfolio spread across different markets, sectors and companies is not immune to political events, but it is less dependent on any single one of them. Time in the market will not make the journey smooth, but it has historically done far more work than trying to trade around every political shock.

Cash still has a role. Everyone needs money for emergencies and short-term spending. But cash is not designed to build long-term wealth. The cost-of-living line on the chart shows the hurdle that inflation quietly creates. Standing still is not the same as keeping pace.

Investing can help your money grow, but the value of investments can rise and fall, so you could get back less than you put in. Investing is for the long term, typically 5 years or more.

A hundred pounds, left alone and given time, can become thousands. The discipline behind that result, patience, conviction and a refusal to be spooked out of the position, is hard to maintain. But for long-term investors, it's key.

This article is for information only and not personal financial advice. If you’re not sure what’s right for you, a financial adviser can help.