Compound Interest

What is compound interest?

Compound interest is the interest added to the balance of a loan or cash deposit, including any interest added in a previous period. This can build over time, creating a ‘snowball’ effect as interest is compounded on interest.

Compound interest applies to liabilities, too. So although it can help boost the value of your cash deposits more quickly, it can also increase the amount of debt charged on a loan when interest builds up on the unpaid interest charges – student loans and mortgages, for example.

What’s the difference between compound and simple interest?

Simple interest is calculated based only on the principal amount, which typically means smaller annual returns over time. On the other hand, compound interest includes both the principal amount and any interest payments added.

Below we consider £1,000 generating 2% a year under simple and compound interest.

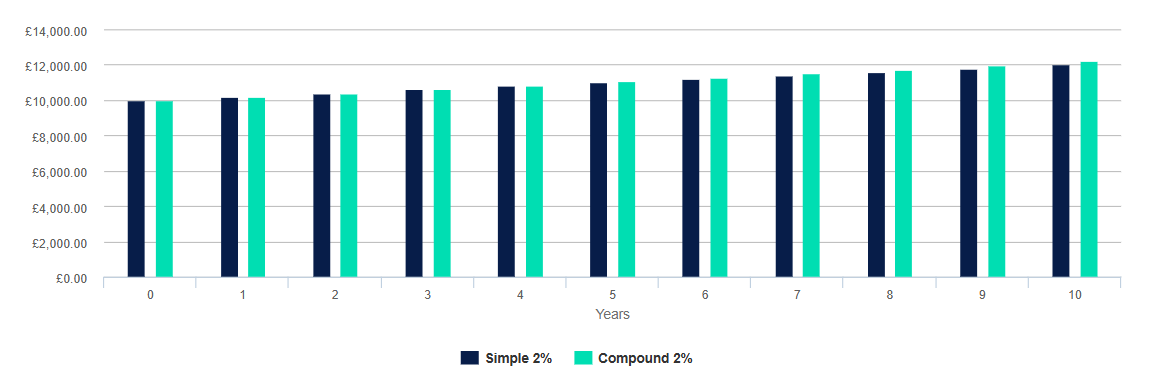

Compounding in the short run

After ten years, simple interest would turn the initial £10,000 into £12,000, simply adding 2% of £10,000 every year. At this point, compound interest is only just starting to pull ahead on £12,190. The difference is small and seemingly insignificant.

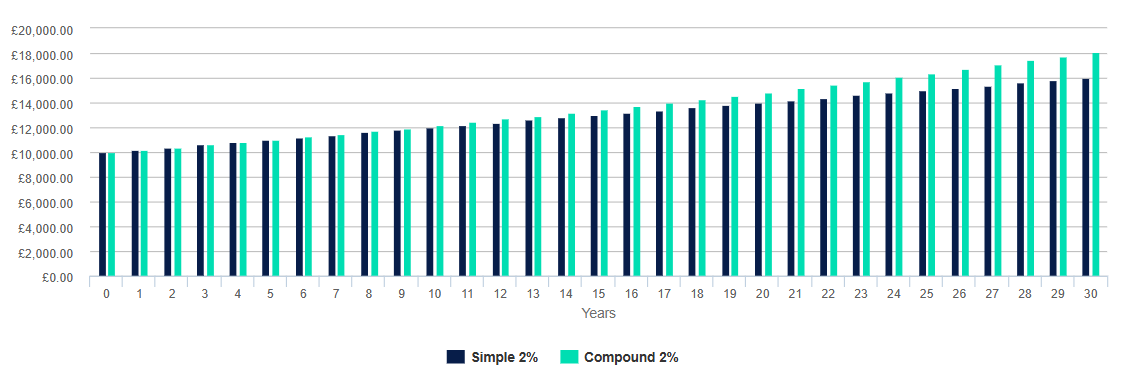

But when we skip ahead to 30 years, we can see where the snowball effect of compounding can really start to gain momentum.

Compounding in the long run

The difference between the two figures is £2,114. That’s the power of compound interest. Clearly, this could be a benefit or a burden depending on whether the interest is working for or against you.

Examples of Compound Interest

Compound interest can be to your benefit or not, depending on whether you’re saving or borrowing money.

Savings accounts and certificates of deposit (CDs). When you deposit money into a bank account that earns interest, such as a savings account, the interest is transferred and added to your account balance. This aids in the development of your balance over time.

Student loans, mortgages, and other personal loans are all examples of debt. When you borrow money, compound interest works against you. If you borrow money and don't pay it back, you will be charged interest. If you don't pay your interest charges within the timeframe specified in your loan, they'll be "capitalised," or added to your original loan sum. Then, interest will be charged on the new, higher loan sum.

How to calculate compound interest

Compound interest can be easily calculated. Suppose the interest annually is 2%, as displayed in the above example. By end of the first year, this amount will be £10,200 with the 2% interest applied (£10,000 x 1.02 = £1,200). The second year, the same interest will be applied to the total amount (£1,200 x 1.02 = £1,404). And so on. The table below illustrates the change in the interest amount year-on-year.

Interest rate 2%

| Year | Amount (£) | Change (£) |

|---|---|---|

| 0 | 10000.00 | - |

| 1 | 10200.00 | 200.00 |

| 2 | 10404.00 | 204.00 |

| 3 | 10612.08 | 208.08 |

| 4 | 10824.32 | 212.24 |

| 5 | 11040.81 | 216.49 |

| 6 | 11261.62 | 220.82 |

| 7 | 11486.86 | 225.23 |

| 8 | 11716.59 | 229.74 |

| 9 | 11950.93 | 234.33 |

| 10 | 12189.94 | 239.02 |

Increased compound periods

The effects of compounding are increased as the frequency of compounding is increased. Consider a one-year time period. The greater the number of compounding periods, the faster the balance increases.

As a result, for savings accounts, two compounding periods per year are better than one, and so forth. But for loans, it’s the opposite.

Let’s compare two different compounding periods, assuming there is a £10,000 loan at an interest rate of 5% per year. Using the formula below:

As illustrated, there’s a £12 increase in the balance when monthly compounding compared with annual compounding in this example.