HL Growth Fund Performance Update – Fourth Quarter of 2025

In this update, we look back at key events impacting the stock market, and how the HL Growth Fund performed between 1 October and 31 December 2025, as well as over longer time periods.

Want to make more of your pension savings? Here we reveal our eight top tips to help you boost your pension savings.

Isabel McDougall, Pensions and Retirement Writer

Last Updated: 12 December 2023

This article isn't personal advice. If you're unsure what’s right for your circumstances, please ask for advice.

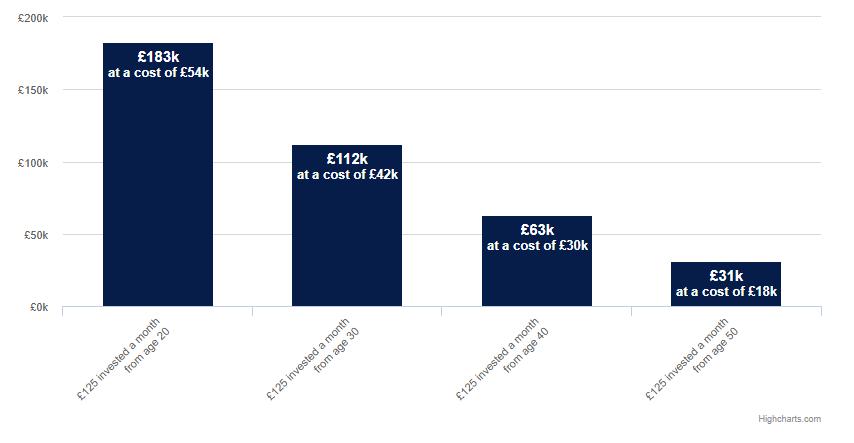

Quite simply, the longer you delay, the more it costs to build a good-sized pension.

This is because of ‘compound interest’, which Albert Einstein reportedly called “the most powerful force in the universe”.

Figures are rounded to the nearest £1000.

Above are four examples of the effect of delay for a non- or basic-rate taxpayer. Let’s assume that you pay £125 a month into a pension until age 65 (which costs you only £100 because the government adds £25 in tax relief). Now say the fund grows 4% a year after charges. What’s the difference if the contribution was started at age 20, 30, 40 or 50? Roughly speaking, every ten-year delay wipes out approximately half of the fund’s potential final value.

These are just projections: the actual return could be less or more than this. The figures don’t take account of inflation, which will reduce the spending power of money over time. Remember, the value of investments can go down as well as up in value, so you could end up with less than you invest.

Everything being equal, the earlier you start saving, the more potential your pension fund has to grow. Explore more detailed figures with our online pension calculator.

If you have a pension, have you ever reviewed it? Many people don't. But it’s important to regularly review your investments and check that they’re still performing as you might have hoped.

Even a seemingly small difference in performance could have a significant impact on the size of the pot. A 35-year-old with a £20,000 pension pot could have a fund worth around £26,800 at 65 if their investments grew by 2% a year. The fund might be worth around £64,000 at 65 if their investments grew by 5% a year or around £149,000 if they grew by 8% a year (in all cases after an assumed annual charge of 1%). Again, these are just projections. Investments will not always go up in value; they can also go down, so you could get back less than you invest. Further to this, these values don’t account for inflation, which will reduce the spending power of money over time.

Many people know how much they pay for their smartphone, but what about for their pension? And do they know what they are paying for?

Pension charges typically buy the services of the pension provider and the expertise of a fund manager who looks after the investments. In addition, some people pay for a financial adviser to make recommendations. The charge for this advice is usually paid separately.

The quality of service provided by one provider to the next may vary. Things that might (or might not) be included:

Good customer service

A helpdesk happy to answer your questions

Quick response times for instructions and enquiries

Online access to the pension

Online planning tools including calculators and portfolio analysis

Clear, concise information

Pension and investment research

As the saying goes: an Englishman’s home is his castle. But it may also be his largest investment. If you decide to use just property as a retirement fund, you might find that you’re putting all your eggs in one basket.

Diversification is key to managing risk, although it doesn’t guarantee that an investor won’t make a loss. So, if you already have capital invested in property, it could make sense for you to consider diversifying and investing in different asset classes.

What’s more, the property market isn’t exactly “safe as houses” – just look at the property crash in 2008.

Our research found that one in three people who have received or are expecting a significant inheritance are banking on it to fund their retirement. But this is an expensive mistake. Life and relationships are impossible to predict, and people shouldn’t be relying on getting a windfall to make ends meet.

We can’t accurately predict how life will turn out for our loved ones. They might end up needing expensive care or spending their money enjoying their retirement to the full. It could leave you with far less than you were expecting, and in some cases, you could end up with nothing at all.

Even if you receive every penny you expect, you have no idea when it might arrive. If they live well into their 90s, you could be 70 before you see any of it. The last thing you want is to be waiting for the death of a loved one to let you do the things you want during your golden years.

The good news is that all UK companies, irrespective of their size, have to provide a pension to their eligible employees and contribute to it on their behalf. The bad news is that some private sector workers aren’t currently saving into a workplace pension. This means that they could be missing out on “free money” from their employer. Many more are contributing just the minimum.

If you have a workplace pension, it’s worth speaking to your employer about paying in more. If you increase your pension contributions, they may pay in more, too. If you’re already contributing the maximum to your workplace scheme, you could consider paying into a private pension like the HL Self-Invested Personal Pension (SIPP). An HL SIPP is for people who want to take control of their retirement savings. You have the freedom to invest exactly where you want to and control how much money goes in and when. Remember, though, that any money in a pension isn’t usually accessible until age 55 (rising to 57 in 2028).

Tax relief on pension contributions is one of those rare occasions when you get tax back. Under current rules, if you pay money into a pension, the government effectively pays 20% of the total contribution (subject to maximum limits).

If you pay a higher rate of tax, you could claim back even more in tax relief. This means that £10,000 in a pension could effectively cost as little as £5,500.

Remember, tax rules can change over time, and the relief received will depend on individual circumstances. Tax bands and rates are different for Scottish taxpayers.

From age 55 (rising to 57 from 2028), up to 25% of a pension can normally be taken as a tax-free lump sum. After that, there are two main ways to draw a taxable income.

If you don’t want to keep your pension invested and worry about the ups and downs of the stock market, you could consider using some (or all) of your pension to buy an annuity. It will provide you with a secure retirement income for life. If you choose this option, make sure you shop around because rates can vary drastically from one provider to the next. And you might not get the best deal with your current pension provider.

Common medical and lifestyle conditions could help increase the annuity income that you could get. It’s not only serious illnesses that qualify.

Another option is drawdown. This is where your pension remains invested and you can take an income from it as and when you need it. It is more flexible – but it is more complex and the income is not guaranteed, so it is riskier.

Alternatively, you can choose to take lump sums directly from your pension. Up to 25% of the lump sum will be tax-free with the rest taxed as income.

How to take money from your pension guide

What you do with your pension is an important decision. We strongly recommend that you understand your options and take appropriate advice or guidance if you are at all unsure. Pension Wise, the Government’s pension guidance service, provides a free impartial service to help you understand your options at retirement and is available for people aged 50 and over.

In this update, we look back at key events impacting the stock market, and how the HL Growth Fund performed between 1 October and 31 December 2025, as well as over longer time periods.

Discover how a financial adviser can guide you through the pension transfer process and offer valuable advice.

Three options to consider when taking tax-free cash from a pension.

Discover how much you might need in retirement, and how much your pension should be worth to achieve your desired income.