The Default Fund

Important information – investing for longer increases the likelihood of positive returns. Over a period of five years or more, investments usually give you a higher return compared to cash savings. But investments can go down as well as up in value, so you could get back less than you put in.

The information in this article is guidance, not personal advice. Learn more about the differences between the two. If you’re still not sure what’s right for you, you should ask for advice. Past performance is not a guide to the future.

Why invest your pension?

At a glance

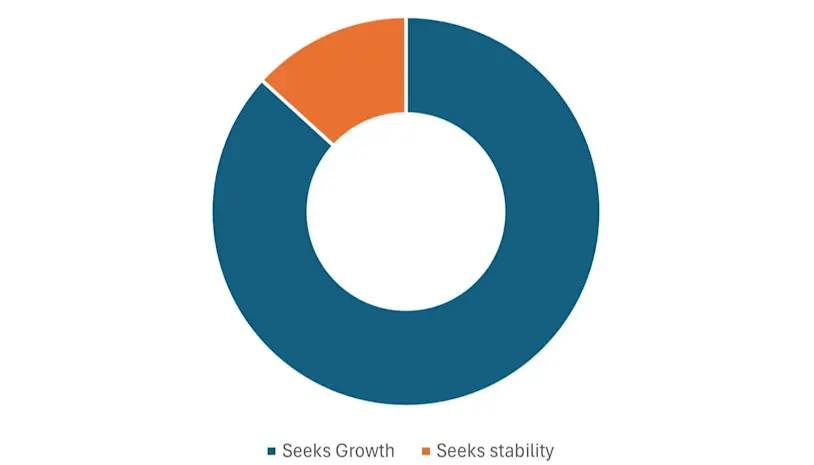

Our experts at HL diversify your pension by selecting a variety of investments from around the globe. This helps to manage how risky your pension is.

It also invests in smaller businesses and ones in emerging markets. These can be higher risk than investing in larger businesses, or those in developed market economies.

For every £5 you invest, just over £4 goes into investments that aim to grow your money over the long term. The rest is invested in areas that add stability to the overall portfolio.

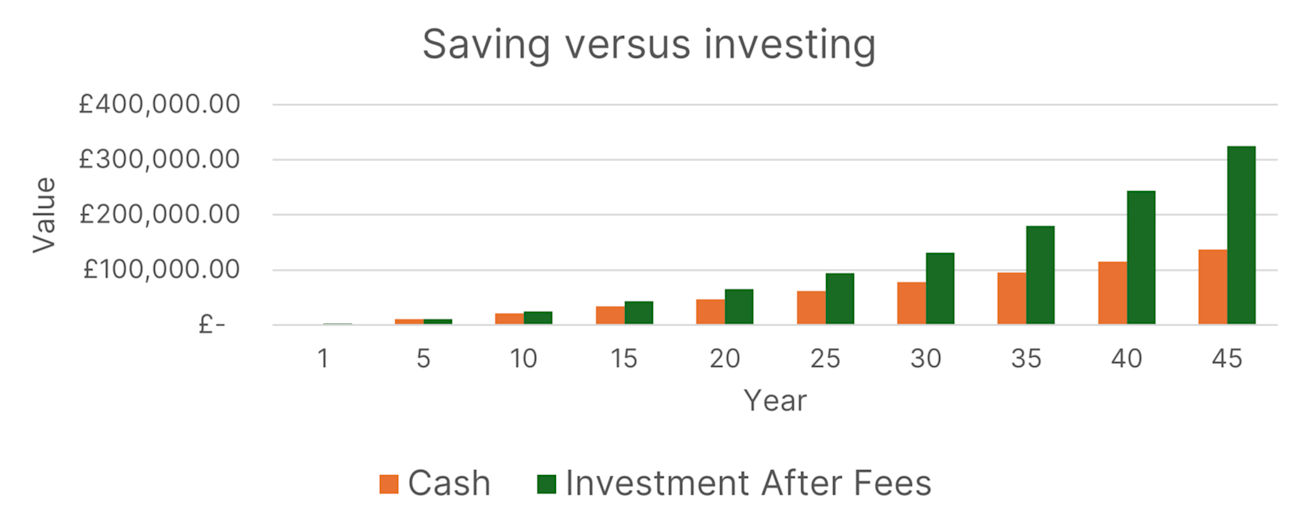

HL Growth Fund expected to significantly outperform cash over 45 years

This chart is for illustrative purposes only, it is not a projection or a guarantee. Source: Moody's & HL, based on fund target asset allocations as at 1 April 2026. We assume no charges for cash, the figures for investing are after deducting the 0.1% fund charge and 0.35% HL account charge. We have taken account of inflation, to show you the values in today’s terms.

The chart above is based on expected returns for cash and the HL Growth Fund. We’ve assumed:

Starting at age 20 and investing for 45 years.

Contributing 8% of salary, starting at £25,000 and rising by 3% per year.

The values shown take account of inflation, so show you what your money could be worth in today’s terms.

When you invest, you can get back less than you put in. But the likelihood of that is reduced dramatically if you invest for longer.

Historically, if you invest for just one year, your chance of losing money is roughly 1 in 5. Invest for five years and it’s 1 in 10. Invest for ten years, and it’s just 1 in 100. Of course, there are no guarantees and past performance isn’t a guide to the future.

What’s your Workplace Pension Default Fund?

How is the HL Growth Fund invested?

At a glance

Our experts at HL diversify your pension by selecting a variety of investments from around the globe. This helps to manage how risky your pension is.

It also invests in smaller businesses and ones in emerging markets. These can be higher risk than investing in larger businesses, or those in developed market economies.

For every £5 you invest, just over £4 goes into investments that aim to grow your money over the long term. The rest is invested in areas that add stability to the overall portfolio.

For illustrative purposes only – actual allocations may vary. Source: LGIM 30 April 2026.

The HL Growth Fund aims to generate the best return possible over long periods of time – 10 years or more – while controlling the overall level of risk.

We do this by selecting a wide mix of investments – including some higher-risk options – giving you the best potential to grow your money, spread broadly across global stock markets for diversification.

This includes investing in smaller companies, and companies based in emerging markets. Over time, these investments offer greater potential for growth, but they are higher risk.

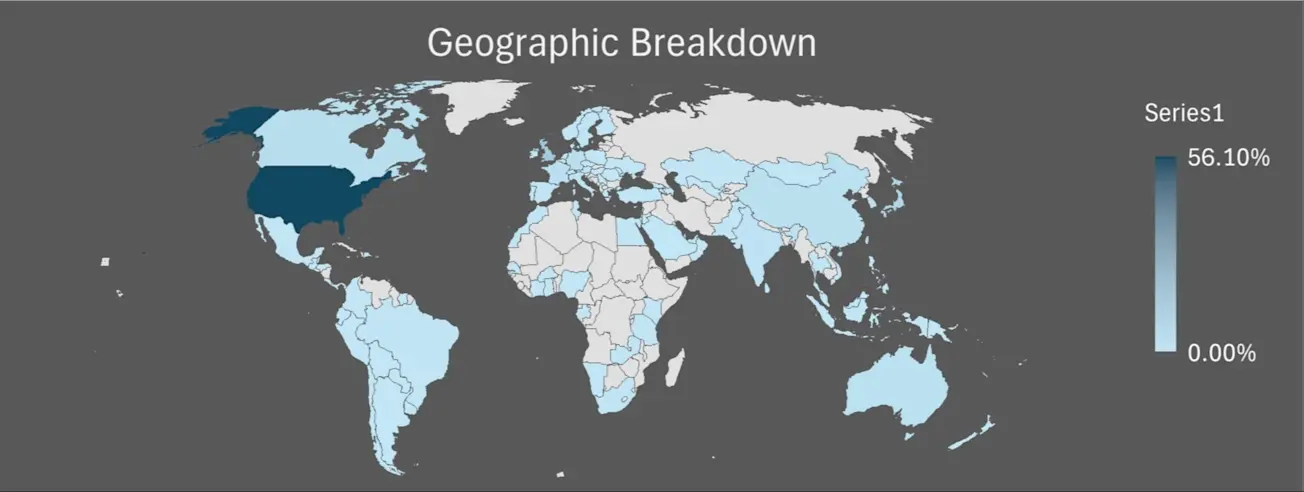

The fund invests mainly in developed markets like the UK, US and Japan.

Spreading your money in this way helps to reduce the risk of any single country’s economy having a dominant impact on your overall returns.

You can see how your money is spread out globally below:

Source: LGIM 30 April 2026.

Country breakdown - How much is invested in each country?

| UNITED STATES | 56.10% |

| JAPAN | 5.89% |

| TAIWAN | 1.90% |

| CANADA | 2.90% |

| AUSTRALIA | 1.78% |

| SWITZERLAND | 1.39% |

| NETHERLANDS | 1.22% |

| Other countries | 8.24% |

| UNITED KINGDOM | 10.21% |

| CHINA | 2.22% |

| FRANCE | 2.43% |

| GERMANY | 2.12% |

| INDIA | 0.93% |

| SOUTH KOREA | 1.68% |

| SWEDEN | 0.98% |

What are the risks?

At a glance

When we decide where to invest on your behalf, we think about risk in two ways:

1. How much you might stand to lose if something goes wrong.

2. How confident we are about what could potentially happen in the future.

We use what we’ve learnt from past drops in the market to help us understand how markets have recovered over time, from different types of stress.

Because the HL Growth Fund holds a variety of investments from around the globe, it’s more diversified than buying individual company shares. This will reduce how risky your Workplace pension is.

On a scale of 1 to 10, if investing entirely in global shares is a 10, the HL Growth Fund would be an 8.5.

How the HL Growth Fund could have performed vs the global stock market in times of crisis

This shows simulated past performance of the HL Growth Fund. Past performance is not a reliable indicator of future performance. Source: HL, based on HL Growth Fund target asset allocation as at 1 April 2026.

On a scale of 1 to 10, and if you invested entirely in global shares, we’d give that a risk rating of 10. The HL Growth Fund has a risk rating of 8.5.

Global stock market

Risk rating (10/10)

Compared to:

HL Growth Fund (Default investment fund)

Risk rating (8.5/10)

We can get a sense of what we might expect by reviewing how different investments have performed in history during times of crisis.

Since the turn of the century there have been several large crashes, like the 2008 global financial crisis or the recent inflation crisis in 2022. Using these examples and by considering the HL Growth Fund’s investment mix, you can see in the chart above how the fund is expected to have performed relative to the global stock market. Remember, past performance isn’t a reliable indicator of future performance.

To understand the risks of investing, we model thousands of possible scenarios to generate forecasts for the fund’s expected returns over the next 10 years.

Our forecasts suggest there is a 1 in 20 chance that the fund could lose 18.7% or more over the next decade – although it’s not a guarantee. Compared to global stock markets and under the same assumptions and scenarios, we think the global stock market could lose 22.5% in the same scenario. This means although losses can be large at times, we expect the HL Growth Fund to offer investors some protection from the worst of market falls.

Although the HL Growth Fund is riskier than playing it “safe” by holding cash, it does offer greater opportunities for growth after considering the effects of inflation. We think that – for investors with a long time to invest – the risk of inflation is greater than the risk of stock market falls when it comes to reaching your goals in retirement.

How much does the HL Growth Fund cost?

At a glance

As an investor, it’s essential to understand all the underlying charges of your investments and the portfolio because it can impact your overall return.

The HL Growth Fund has an ongoing charge of 0.1% each year.

It’s one of the lowest-cost investments available to clients who hold a Workplace pension through HL.

The fund charge is in addition to the platform charge of up to 0.35%. Total annual cost is just £5.50 for every £1,000 you invest.

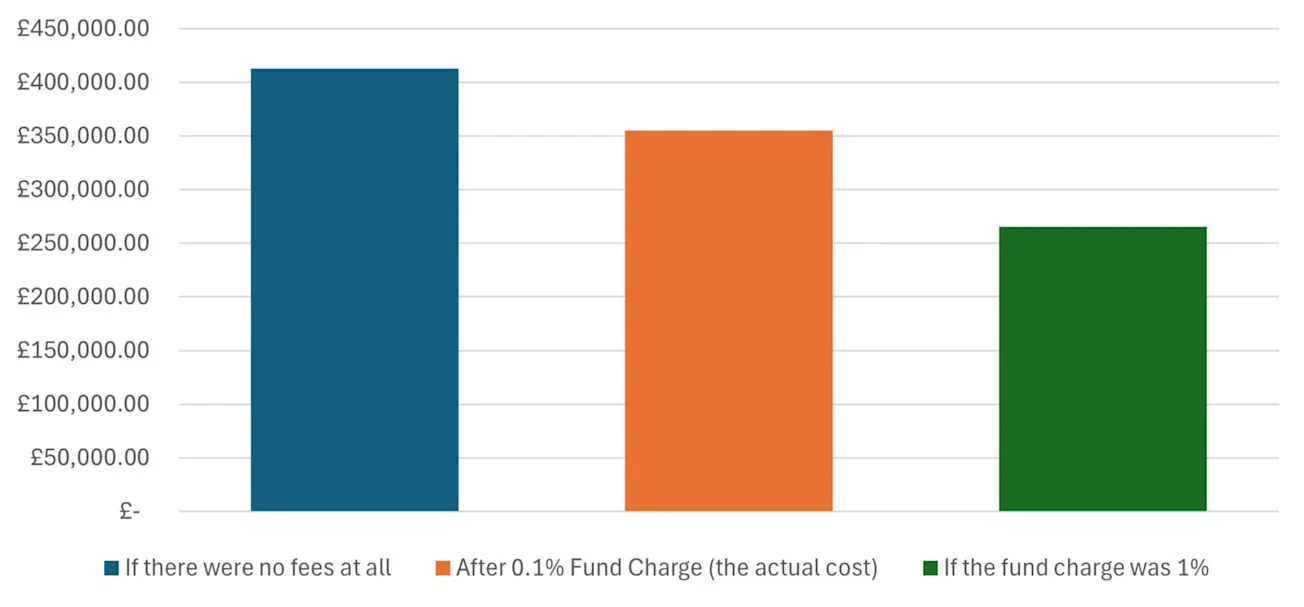

Charges can have a big impact on your overall return. For example:

The effect of fund charges on the value of an investment

After contributing for 45 years, this employee could expect to have a pension pot worth around £355,300 in today's terms with a 0.1% fund charge. If the fund charge was 1%, and performance stayed the same, they would only expect to receive around £265,400. Both examples assume a platform charge of 0.35% in addition to the fund charge.

Source: HL. Based on an 8% annual contribution and a starting salary of £25,000, which rises annually by 3%. We have accounted for inflation to show the values in today's terms. Investment illustrations take account of the fund and platform charges, whereas the example without any charges does not consider any fees.

Next steps

If you’re happy with the aims and objectives, charges and risks of the HL Growth Fund, just make sure you’re logging in to your pension account regularly to check its progress. We think every six months is sensible.

If you’d like to make changes to your investments, or explore your options in more detail, we can help. Find out more information about the HL Starter Funds – the next step in your investment journey.

HL Growth Fund updates

Every three months, our investment specialists publish a paper on how recent global and local events have impacted the performance of the HL Growth Fund.