HL Growth Fund Performance Update – Fourth Quarter of 2025

In this update, we look back at key events impacting the stock market, and how the HL Growth Fund performed between 1 October and 31 December 2025, as well as over longer time periods.

Annuity rates have risen again, is it time to re-examine your retirement plans? Find out why drawdown investors could consider buying an annuity.

Isabel McDougall, Pensions Writer

Last Updated: 6 September 2023

This article is archived

The content is over 90 days old. It was correct at the time of publishing. Our views and any references to tax, investment, and pension rules may have changed since then.

An annuity remains one of the only ways to turn your pension into a guaranteed income for life. But over the years, the amount of annuity income you can buy with your pension has been falling, making them a less popular retirement option.

It’s likely that for many drawdown investors, annuity rates were unattractive at the time they started taking money from their pension. Keeping their pension invested and taking a flexible income may have seemed more appealing.

But with average annuity rates having risen again, now could be a great time for drawdown investors to re-examine their retirement options.

This article isn't personal advice. Annuity rates change regularly, and quotes are guaranteed for only a limited time. If you're not sure what to do with your pension, you should seek guidance from Pension Wise, the government’s free impartial service to help you understand your retirement options. If you need more help, you could consider financial advice.

It’s often overlooked by retirees that you can swap some, or all, of your pension for an annuity, even if you’ve already taken your tax-free cash or drawn an income. After all, retirement isn’t all or nothing.

The first step is to understand your annuity options. For example, you can choose to inflation-proof your annuity income. Or you can opt for your loved ones to receive an income after you've passed away. Then, you’ll need to get an annuity quote to find out how much guaranteed income you could get each year.

It's free to get a quote and will take only a few minutes with our annuity calculator. All you need to do is answer some questions about yourself and your pension. Our calculator will search the UK market to work out who will give you the best annuity rate.

You cannot take more tax-free cash from funds already in drawdown. So make sure you select the ‘no tax-free cash’ option when you get a quote.

More on annuity options More on buying an annuity

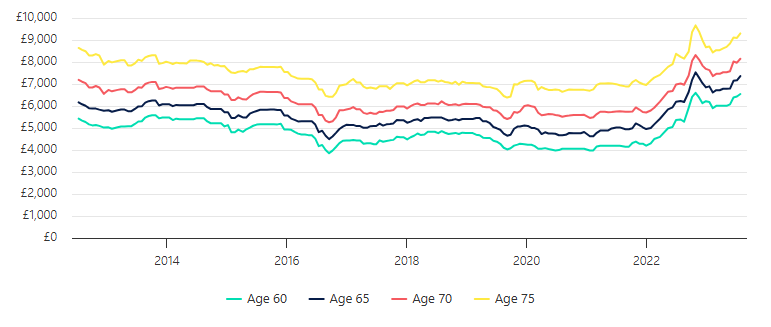

Last October, annuity rates were the highest they’ve been in more than 14 years. In fact, annuity rates have jumped by almost 50% in two years. Someone aged 65 with a £100,000 pension can now get an annuity income of £7,358*. The same time two years ago, the best rate they could have received was £4,946. That’s about an extra £2,400 every year. Across 10 years, that’s a whopping £24,000 more.

Just look at the graph below to see how rates have changed over the years.

Source: : *HL annuity index, 27/07/2023. This index tracks the top rate for a single life, level annuity, paid monthly in advance with a five-year guarantee period and a £100,000 purchase price. Postcode PE29 7HG. Rates up to 21/12/2012 are for a 65 year old male and after that are unisex.

The income you could receive will depend on your circumstances. Quotes are guaranteed for only a limited time. Rates change frequently and could go up or down in the future. It's also important to consider your options carefully as you can't usually change or cancel an annuity once it's set up.

It’s always a good idea to keep an eye on annuity rates. Although rates are close to the highest they’ve been in years, they will change in future. Rates could go up further or down.

A good way to help protect against losing out either way is to buy several smaller annuities in stages. This means that you won’t lock all your money into an annuity rate at one point in time and you’ll keep the flexibility that your drawdown pension offers. This approach lets you gradually reduce risk from your pension throughout your retirement, which could help to give you peace of mind during uncertain times.

Let’s say you bought an annuity now, you could lock in some guaranteed income at a rate that’s close to the highest we’ve seen in years. And if raites rise again in the future, you can buy more at that point. If rates fall again, you haven’t missed out.

There’s no obligation to buy an annuity after you’ve searched for quotes, but any rate on the quote will be guaranteed for only a limited time.

Once you buy an annuity, the income it pays is fixed for the rest of your life. It will change only if you build in certain annuity features such as a guarantee period or opting for a beneficiary’s pension, so make sure you consider your annuity options carefully.

Don’t just accept the first annuity quote you find. Rates vary between providers and your current pension provider might not offer you the most for your money. It’s always worth shopping around to get the best deal.

Unlike some insurance products, if you disclose your health and lifestyle details when you get an annuity quote, you’ll normally get a better deal. Even confirming minor details like your height and weight could mean that you get a higher annuity income. This type of annuity is known as an enhanced annuity.

In this update, we look back at key events impacting the stock market, and how the HL Growth Fund performed between 1 October and 31 December 2025, as well as over longer time periods.

Discover how a financial adviser can guide you through the pension transfer process and offer valuable advice.

Three options to consider when taking tax-free cash from a pension.

Discover how much you might need in retirement, and how much your pension should be worth to achieve your desired income.