HL Growth Fund Performance Update – Fourth Quarter of 2025

In this update, we look back at key events impacting the stock market, and how the HL Growth Fund performed between 1 October and 31 December 2025, as well as over longer time periods.

HL client Mr Boyce shares his strategy for becoming a pension millionaire and early retiree Mr Adlam shares his experience of building a healthy pension. Plus, we look at 8 tips to boost the value of your pension.

Isabel McDougall, Pensions Writer

Last Updated: 6 April 2024

Reaching a million-pound pension is challenging for any pension investor, but it's not impossible. Over 1,800 HL clients have a Self-Invested Personal Pension (SIPP) value over £1,000,000.

But what's their secret?

Mr Boyce and Mr Adlam share their stories below, and we highlight eight pension-boosting tips.

This article is designed to give you useful information, but it's not personal advice. If you're not sure what's right for your circumstances, ask for financial advice. Investments fall as well as rise in value, so you could get back less than you invest. The information in this article applies to the 2023/24 tax year.

It's time in the market, not timing the market

Mr Boyce

I started saving into a pension early - from age 20. Luckily, every company I have ever worked for has had a workplace pension of some sort which I've been able to take advantage of.

When it comes to saving for retirement, my top tips would be to start early, and put in as much as you can. People have misconceptions about pensions. Many people think it's ok to start later and put off saving until they're older. But it's true what they say, the earlier you start, the better off you could be.

Once I had built up pension pots with different providers, I decided to consolidate them into an HL Self-Invested Personal Pension. I wanted to have a crack at managing my pensions myself. There are many things I like about the HL Self-Invested Personal Pension: the wide range of investment options, the research and tools on offer, the expertise and insight from investment analysts, the option to take advice if I need it.

My top tips for SIPP investors would be – remember this, it's time in the market, not timing the market. Also, don't listen to friends' tips: for the one that makes you money, there will be ten that don't.

When it comes to investing, I think it's important to do your own research, and don't buy anything you don't understand. It's also important to take stock of your investments regularly. I rebalance my positions once or twice a year."

Don't invest in anything you don't understand

Mr Adlam

I started saving for retirement early – at age 27. I had a workplace pension, and I could choose how much to save. I paid in the maximum, which I think was 6% of my salary at the time and my employer matched this. Retirement felt like such a long way off, and several times I questioned myself if I was doing the right thing, but I'm glad I did.

Once I hit age 40, I started increasing my pension contributions. I could see that even small pension increases early would have time to really grow my pension pot over time.

My top saving tip is simple. Start early. I'm now at 56 and having just taken early retirement, I'm reaping the rewards.

I think the key to successful investing is doing your own research and don't invest in anything you don't understand. Also remember that investing is for the long term."

Becoming a pension millionaire might not be possible for everyone. But if you want a fighting chance, you'll need to commit to some smart saving and good investment habits.

You'll likely need to make some sizeable pension contributions to become a pension millionaire. But the sooner you start saving, the more time you'll have to reach your goals.

Here are some examples of how much your pension could be worth by the time you're 68 if you pay in £300 a month (increasing by 3% each year), depending on when you start. These figures are based on assumed annual growth of 5% after any charges. They also don't take inflation into account. These figures are an illustration, and what you get will depend on several factors including your investment performance.

Starting at 25 years old:

| Monthly contribution | Pension value at 68 |

|---|---|

| £300 a month (increasing by 3% a year) | £847,000 |

Starting at 30 years old:

| Monthly contribution | Pension value at 68 |

|---|---|

| £300 a month (increasing by 3% a year) | £611,000 |

Starting at 35 years old:

| Monthly contribution | Pension value at 68 |

|---|---|

| £300 a month (increasing by 3% a year) | £435,000 |

Find out how much my pension could pay

If you can afford to, it can make sense to increase your contributions regularly.

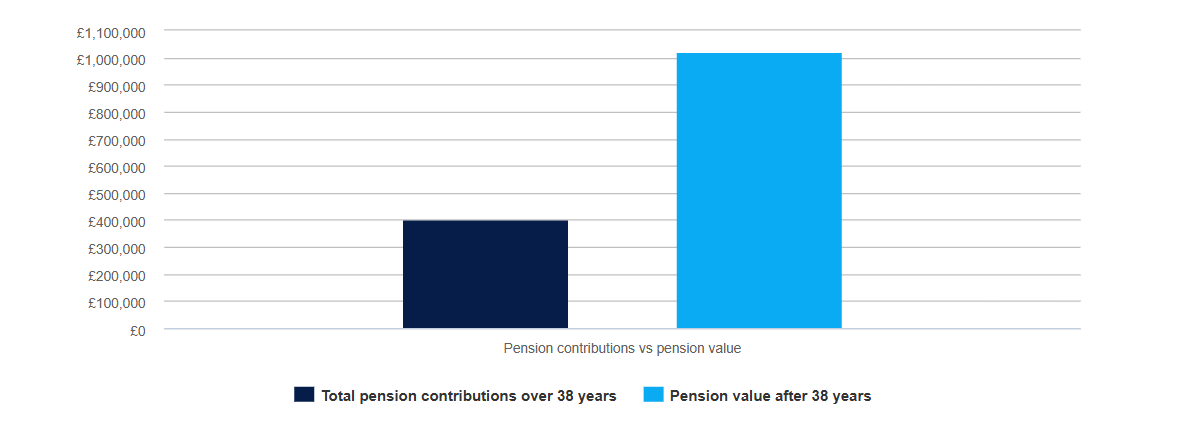

The examples in Tip 1 assume contribution increases of 3% each year. But imagine that you start investing £300 a month in a pension from age 30 and increase your contributions by 6% (as you get older and potentially earn more). You could end up with a pension worth over £1 million at age 68. In this example, you would've invested only just over £400,000.

As with the figures in Tip 1 above, this assumes investment growth of 5% a year after charges. It doesn't consider inflation, which erodes the value of money over time.

If you have a workplace pension, your employer will be making regular contributions into it. One potential quick win is to find out the maximum your employer will pay in and make sure you're taking advantage of that opportunity, if you’re able to.

Although many employers pay only the minimum set out under auto-enrolment rules (pension contributions equal to 3% of your qualifying earnings), others are willing to pay more. Your employer could be, too.

Making a larger contribution – even as a one-off – can have a significant impact on your retirement fund. And if left invested for several years, it could leave you with a much larger pension than you otherwise would have.

If you decide to significantly boost your pension, you could pay in more than £60,000, by using unused allowance from previous years, provided you also have sufficient earnings. This is known as the carry forward rule.

Career breaks often mark the start of a major life change like starting a family or looking after an elderly relative. But it's important your pension doesn't fall off the agenda.

Stopping your pension contributions for even a relatively short time could have a huge impact on your retirement savings. If you're taking a break to go on paid parental leave, it could pay to keep your pension contributions going if you can. That's because your contributions will normally be based on your actual earnings during that period (which are likely to be lower). But any employer contributions will continue to be based on the level of earnings you were getting before.

You can usually access a pension from age 55 (rising to 57 in 2028). You can normally take up to 25% tax-free (up to a maximum of £268,275) and the rest is taxable.

Many people choose to access their tax-free cash to pay off expenses, like a mortgage or to make a big purchase. But if you can afford to, it makes sense to leave your pension untouched until you plan to retire.

There used to be a limit to the total value of pension benefits you could build up throughout your lifetime and generally receive up to 25% tax free. This limit was known as the lifetime allowance and was set at £1,073,100 for most people. However, from 6 April 2024, the lifetime allowance was abolished and replaced with three new allowances. These are the lump sum allowance, the lump sum and death benefit allowance, and the overseas transfer allowance.

To find out more about the new allowances, including how you may be affected if you used lifetime allowance under the previous rules, visit our dedicated webpage.

Around £27bn has been left unclaimed in the UK. If you've moved jobs or changed address, you could have an old pension waiting to be found.

If you're hoping to build up a sizable retirement pot, check the whereabouts of all your old pensions and claim back any that have been misplaced. It could be a good idea to then bring them all together into one easy-to-use account like the HL SIPP.

In this update, we look back at key events impacting the stock market, and how the HL Growth Fund performed between 1 October and 31 December 2025, as well as over longer time periods.

Discover how a financial adviser can guide you through the pension transfer process and offer valuable advice.

Three options to consider when taking tax-free cash from a pension.

Discover how much you might need in retirement, and how much your pension should be worth to achieve your desired income.