HL Growth Fund Performance Update – Fourth Quarter of 2025

In this update, we look back at key events impacting the stock market, and how the HL Growth Fund performed between 1 October and 31 December 2025, as well as over longer time periods.

The Bank of England cut interest rates from 4.75% to 4.5%. In this article we’ll find out what this means for annuities.

Isabel McDougall, Pensions Writer

Last Updated: 9 April 2025

An annuity remains one of the only ways to turn your pension into a guaranteed income for life. Annuity rates determine how much guaranteed income you can get when you swap some, or all, of your pension pot for a secure income. These rates change regularly, and they're calculated based on several different factors, like the value of your pension. They are also strongly influenced by interest rates.

The Bank of England has cut interest rates from 4.75% to 4.5% - the lowest base rate since June 2023. The recent rate cut will likely do little to dampen demand, with annuities expected to deliver great value to retirees for some time yet.

This article isn't personal advice. If you're not sure what type of pension you have, or what to do with it, you should seek guidance from Pension Wise. If you need more help, you could consider financial advice.

Annuity providers typically buy government bonds to generate returns. High interest rates push these returns up. So a rise in interest rates should push annuity rates up as a result.

Find out how much secure income you could get

Equally, when interest rates are low, bond returns are typically lower which means annuity rates have also tended to be lower. For example, when the Bank of England slashed the UK base rate to the lowest level in history (0.1%) on 19 March 2020, two annuity providers dropped their rates. The best standard payout for a 65-year-old also reduced by around 4%.

Annuity rates have generally been fluctuating over the past two years but income continues to hover just below all-time highs. In November 2024 a £100,000 pension pot could have bought an annuity of £7,499 – the highest within the past two years. Whereas at the beginning of February 2025 the same amount can buy an annuity of £7,490 a year, slightly less than the all-time high.

The quotes above are for a married 65-year-old and were based on a single life level annuity, with a 5-year guarantee and income being paid monthly in advance. The income you could receive will depend on your circumstances. Quotes are only guaranteed for a limited time and rates change frequently. They could go up or down in the future. It's also important to consider your options carefully as you can't usually change an annuity once it's set up.

Interest rates aren't the only thing affecting the income you can receive.

Providers change their rates all the time. And the provider offering the highest income is constantly changing. This means shopping around is vital. Your current provider might not offer you the best deal.

You can get quotes from all the main annuity providers in the UK using our annuity quote tool.

Get an annuity quote See the best annuity rates

Annuity providers decide your income based on how long they think you will live. The longer you are expected to live, the longer they'll need to pay you.

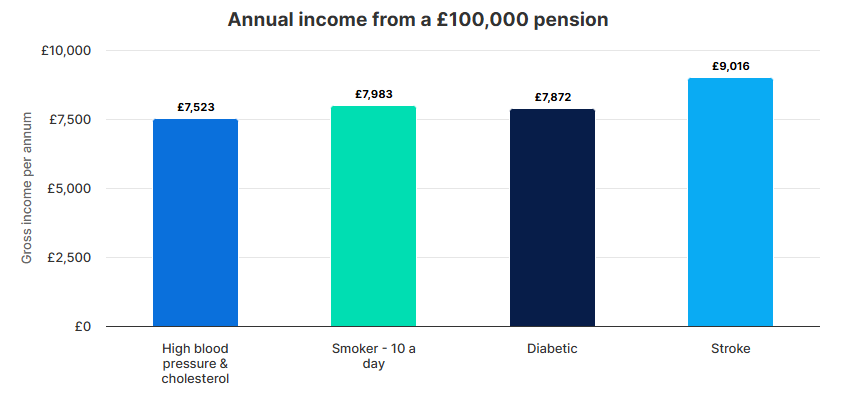

Anything that might mean your life expectancy is reduced could mean you get more income. Just look at the graph below.

We generated these quotes using our online annuity quote tool on 18 March 2025. All quotes are for a single life annuity, paid monthly in advance, with no escalation or guarantees built in. Quotes are for a married man aged 65 with a wife 3 years younger, who lives in an area which has an average life expectancy. When health details have been added, we've also said they drink 7 units of alcohol a week and have a Body Mass Index of 27. These are known as enhanced annuities. You can confirm health information when you request a quote to see how much more income you could get. Annuity rates change all the time, so they could be higher or lower in the future.

You don't need to have health conditions to qualify for a higher rate. Even confirming your height, weight and alcohol intake could mean you get more income.

More on enhanced annuitiesFind out how much annuity income you could receive

Pension Wise is a free, impartial government service for anyone aged 50 or over, with a UK-based personal or workplace pension.

It can help you understand what type of pension you have, how you can access your savings and the potential tax implications of each option. But it isn't financial advice.

We offer a range of information and support to help you plan your own finances. Our team of highly qualified financial advisers can help you achieve your goals. Our flexible approach means you only pay for the advice you need.

If you'd like to get annuity quotes over the phone and discuss your options with one of our retirement experts, our UK-based helpdesk is here for you six days a week. Our friendly and knowledgeable team is ready to answer your questions no matter how big or small. Call 0117 980 9940 (Monday- Friday 8am-5pm and Saturday 9:30am-12:30pm).

In this update, we look back at key events impacting the stock market, and how the HL Growth Fund performed between 1 October and 31 December 2025, as well as over longer time periods.

Discover how a financial adviser can guide you through the pension transfer process and offer valuable advice.

Three options to consider when taking tax-free cash from a pension.

Discover how much you might need in retirement, and how much your pension should be worth to achieve your desired income.