Investment Risk

How to manage your investment risk

Important information - This page is designed as guidance to help you manage your risk, not personal advice. Learn more about the differences between the two. If you’re still not sure what’s right for you, then you should ask for advice. All investments and any income they produce can fall as well as rise in value, so you could get back less than you invest. Past performance is not a guide to the future.

What you need to know

At a glance

Investment risk comes with the potential for reward. But more risk can also mean more of a chance of losing what you initially invested.

Some investments are riskier than others.

There are different types of risk to think about when you invest.

What is investment risk?

When you invest, there’s a risk that your investments could fall in value and that you get less back than you initially invested.

All investments will rise and fall in value – how much they move and how often (their volatility) help to determine how risky they are.

Over the long term, investments have typically tended to go up, as long as you’re willing to be patient and ride out these ups and downs.

It’s never a certainty and, depending on the investment, it can be a bumpy ride. Taking on more risk could give you more reward – but bigger potential losses.

Different types of risk

Risk has lots of definitions. To keep things simple, we can broadly split it up into two main categories:

Risk of loss – all investments carry some degree of risk so it’s possible you could get back less than you invest. It’s the risk you take when investing – you’ll need to be comfortable with this if you’re looking to grow your wealth by investing.

Volatility risk – this is the most common way to measure risk. It measures how regularly and abruptly prices swing. If the price stays fairly stable, the investment has low volatility. If the price bounces around a lot, the investment has high volatility. Riskier investments are nearly always more volatile which means they reach new highs and lows very quickly.

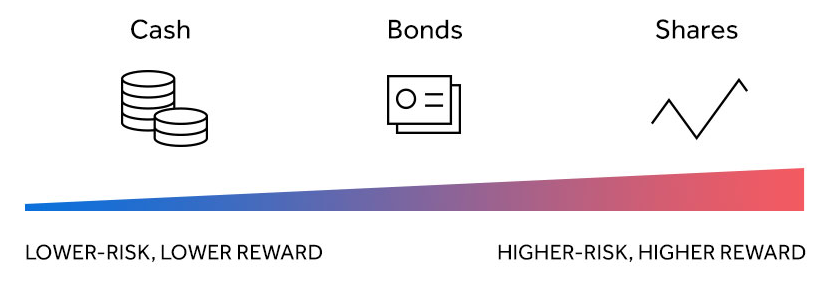

Risk and reward

Every investment carries a different level of risk. Cash is low risk but low reward while shares tend to be the opposite.

While higher-risk investments, such as shares, are expected to produce a higher return over the long term, their potential to lose value is generally higher too.

How to manage risk

At a glance

Think about how to manage your risk through an investment strategy.

Try to manage what you can control when you invest – there will be some things you can’t.

The size of a company matters when you invest, but only in relation to your long-term investment goals.

Avoid following the crowd – make investment decisions on your own terms.

How to manage investment risk

Diversification

There will always be ups and downs in the value of your investments as markets move. To try to have something working in your favour and smooth out the ride, you diversify your investments. Then, if one investment goes through a bad patch, ideally there will be others doing well.

Long-term investing

Investments tend to perform better over the long term. Any bumps in the road are smoothed out as the stock market has time to bounce back. Remember, though, investing doesn’t come with any guarantees.

Less than 5

If your time horizon is less than five years, you should keep your money tucked away in cash savings. Just make sure you shop around for the best rates – the Active Savings service could help.

5 - 10 years

If you are investing for five to ten years, then you might want to take a more cautious approach. Market drops can be damaging for investors with a shorter timeframe. It could lead to selling your investments at a market low point when you need to access your money.

10+ years

If you’re investing for 10 years or more and retirement isn’t on the horizon, you could be more adventurous with your investments. Just make sure that you’re comfortable with the higher risks.

The more time, the better. It gives you a better opportunity to reap the rewards of compounding – arguably the number-one weapon in an investor's toolbox.

More on investing for the long term

Invest into funds – funds offer an easy and convenient way to invest, popular with novice and experienced investors alike. They’re a collection of investments chosen and run by a fund manager, so you benefit from the knowledge, skills, and experience of a professional. With thousands of funds available, you can invest in a mix of asset types such as shares and bonds to spread the risk around.

Risk - what you can and can't control

What you can control:

How well you’ve diversified your portfolio - Diversification is a tool to help you manage risk, when you have no way of knowing what’s going to happen.

Staying invested long term - That’s at least 5 to 10 years. If you take your money out by reacting to short-term noise, you risk buying investments back at the wrong times.

What you can't control:

Short-term noise and what’s going on in the news - What’s going on around us causes us to make decisions – but it doesn’t mean they’re the right ones for your personal goals.

How your investments perform - Stock markets are unpredictable, and you won’t always get things right. Although, holding a mixed bag could mean you’ve always got something performing well.

Does company size matter?

Yes, not all risk is equal – some companies carry more risk than others. It’s essential to understand the companies you could invest in and how they impact the balance and overall risk level of your portfolio.

It’ll dictate the size and scale of the ups and downs your investment portfolio might face.

Listed companies' shares come in all shapes and sizes, from small, innovative start-ups to larger, well-established market leaders. These can be broken down into two styles:

Small companies

Focused on growth

Smaller market capitalisation (value of a company that’s traded on the stock market), so have a lower market value

Domestically focused – they could be affected more by downturns to the economy

In narrow industries or niche fields, so there could be some exciting opportunities

Prices are more likely to rise and fall more often, which can be riskier

Large companies

Bigger market value and carry some of the biggest names

Tend to be leaders in their sector and generate profit from a larger base, globally or through wider product range

Can be harder for these companies to grow

Sometimes reward investors with dividend payments – income is never guaranteed, though

The FTSE 100 Index in the UK is made up of the 100 biggest companies and includes companies like Tesco, Lloyds, or Rolls Royce

The size of companies you invest in can affect your expected returns and expected volatility (the ups and downs in the value of your investments).

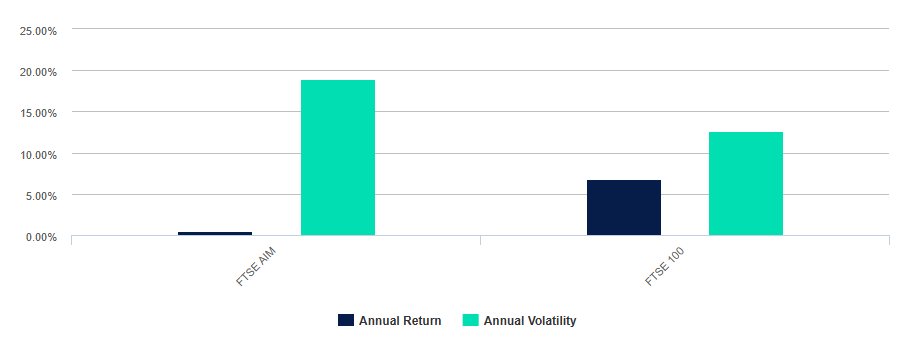

The below chart shows how volatility and returns can vary between shares of different sizes.

A comparison between the FTSE 100 and FTSE AIM indexes between 2004 and 2024

Past performance isn’t a guide to the future. Source: Eikon. Correct to 31/12/2024.

The FTSE AIM index has been the worst performing UK index between 2004 and 2024. This is home to small and medium-sized UK growth companies – they’re seen as riskier, but that hasn’t meant they’ve produced a better return collectively.

Past performance isn’t a guide to the future. Source: Eikon. Correct to 31/12/2024.

We think it’s important for investors to weigh up both the potential risks and rewards to make sure any investments add to a diversified portfolio, for the long term – at least 5 years.

Avoid following the crowd

Herd mentality is where people act in the same way or copy the actions of others, often putting aside their own feelings in the process.

Investors can gravitate towards fashionable stocks, not because they’re the best investment opportunities, but because that’s what the masses are buying. They speculate on short-term popularity and fear they’ll miss out on profits others could be making.

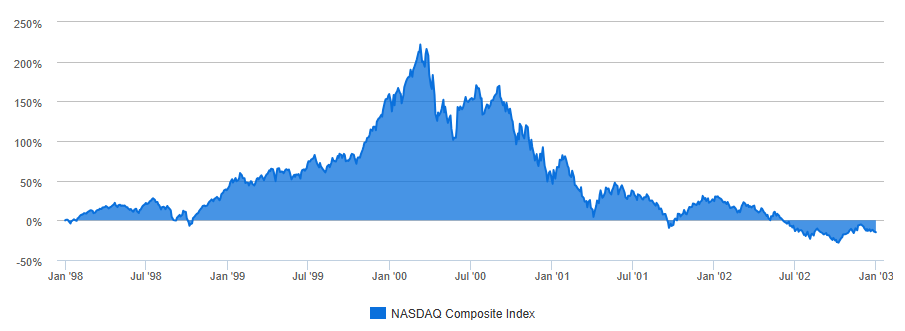

One famous example is the dot-com bubble (or internet bubble). In the late 1990s and early 2000s, many investors flocked together to pump billions into small technology-based companies in an attempt to cash in on the internet boom.

Past performance isn’t a guide to the future. Source: Lipper IM, to 31/12/2002.

As more and more investors piled into the tech market – the bubble eventually burst.

The internet start-up stocks didn’t live up to their hype, and investors lost patience. The tech-heavy US index the NASDAQ Composite rose and fell by more than 200% between 1997 and 2002 – surrendering all its gains made during the bubble.

Following the herd and making investment decisions based on what others are doing is rarely a recipe for success. You shouldn’t feel pressured to invest into high-risk assets, like cryptocurrencies, just because you see others doing it. Remember, investments should be a long-term thing, not a get-rich-quick scheme.

Ultimately, avoiding the herd mentality allows you to make your own decisions that align with your investing goals and risk appetite.

How much risk is right for you?

At a glance

Make sure you know why you’re investing – be clear on your goals.

Consider how long you’re investing for. Different goals will need different lengths of time to stay invested.

Risk is inevitable in investing. It’s how you handle it that matters.

How to manage investment risk

Diversification

There will always be ups and downs in the value of your investments as markets move. To try to have something working in your favour and smooth out the ride, you diversify your investments. Then, if one investment goes through a bad patch, ideally there will be others doing well.

Long-term investing

Investments tend to perform better over the long term. Any bumps in the road are smoothed out as the stock market has time to bounce back. Remember, though, investing doesn’t come with any guarantees.

Less than 5

If your time horizon is less than five years, you should keep your money tucked away in cash savings. Just make sure you shop around for the best rates – the Active Savings service could help.

5 - 10 years

If you are investing for five to ten years, then you might want to take a more cautious approach. Market drops can be damaging for investors with a shorter timeframe. It could lead to selling your investments at a market low point when you need to access your money.

10+ years

If you’re investing for 10 years or more and retirement isn’t on the horizon, you could be more adventurous with your investments. Just make sure that you’re comfortable with the higher risks.

The more time, the better. It gives you a better opportunity to reap the rewards of compounding – arguably the number-one weapon in an investor's toolbox.

More on investing for the long term

Invest into funds – funds offer an easy and convenient way to invest, popular with novice and experienced investors alike. They’re a collection of investments chosen and run by a fund manager, so you benefit from the knowledge, skills, and experience of a professional. With thousands of funds available, you can invest in a mix of asset types such as shares and bonds to spread the risk around.

Risk - what you can and can't control

What you can control:

How well you’ve diversified your portfolio - Diversification is a tool to help you manage risk, when you have no way of knowing what’s going to happen.

Staying invested long term - That’s at least 5 to 10 years. If you take your money out by reacting to short-term noise, you risk buying investments back at the wrong times.

What you can't control:

Short-term noise and what’s going on in the news - What’s going on around us causes us to make decisions – but it doesn’t mean they’re the right ones for your personal goals.

How your investments perform - Stock markets are unpredictable, and you won’t always get things right. Although, holding a mixed bag could mean you’ve always got something performing well.

Does company size matter?

Yes, not all risk is equal – some companies carry more risk than others. It’s essential to understand the companies you could invest in and how they impact the balance and overall risk level of your portfolio.

It’ll dictate the size and scale of the ups and downs your investment portfolio might face.

Listed companies' shares come in all shapes and sizes, from small, innovative start-ups to larger, well-established market leaders. These can be broken down into two styles:

Small companies

Focused on growth

Smaller market capitalisation (value of a company that’s traded on the stock market), so have a lower market value

Domestically focused – they could be affected more by downturns to the economy

In narrow industries or niche fields, so there could be some exciting opportunities

Prices are more likely to rise and fall more often, which can be riskier

Large companies

Bigger market value and carry some of the biggest names

Tend to be leaders in their sector and generate profit from a larger base, globally or through wider product range

Can be harder for these companies to grow

Sometimes reward investors with dividend payments – income is never guaranteed, though

The FTSE 100 Index in the UK is made up of the 100 biggest companies and includes companies like Tesco, Lloyds, or Rolls Royce

The size of companies you invest in can affect your expected returns and expected volatility (the ups and downs in the value of your investments).

The below chart shows how volatility and returns can vary between shares of different sizes.

A comparison between the FTSE 100 and FTSE AIM indexes between 2004 and 2024

Past performance isn’t a guide to the future. Source: Eikon. Correct to 31/12/2024.

The FTSE AIM index has been the worst performing UK index between 2004 and 2024. This is home to small and medium-sized UK growth companies – they’re seen as riskier, but that hasn’t meant they’ve produced a better return collectively.

Past performance isn’t a guide to the future. Source: Eikon. Correct to 31/12/2024.

We think it’s important for investors to weigh up both the potential risks and rewards to make sure any investments add to a diversified portfolio, for the long term – at least 5 years.

Avoid following the crowd

Herd mentality is where people act in the same way or copy the actions of others, often putting aside their own feelings in the process.

Investors can gravitate towards fashionable stocks, not because they’re the best investment opportunities, but because that’s what the masses are buying. They speculate on short-term popularity and fear they’ll miss out on profits others could be making.

One famous example is the dot-com bubble (or internet bubble). In the late 1990s and early 2000s, many investors flocked together to pump billions into small technology-based companies in an attempt to cash in on the internet boom.

Past performance isn’t a guide to the future. Source: Lipper IM, to 31/12/2002.

As more and more investors piled into the tech market – the bubble eventually burst.

The internet start-up stocks didn’t live up to their hype, and investors lost patience. The tech-heavy US index the NASDAQ Composite rose and fell by more than 200% between 1997 and 2002 – surrendering all its gains made during the bubble.

Following the herd and making investment decisions based on what others are doing is rarely a recipe for success. You shouldn’t feel pressured to invest into high-risk assets, like cryptocurrencies, just because you see others doing it. Remember, investments should be a long-term thing, not a get-rich-quick scheme.

Ultimately, avoiding the herd mentality allows you to make your own decisions that align with your investing goals and risk appetite.

Investment ideas for each account

If you’re not sure where to get started, our experts have chosen some investment ideas for our different accounts. But remember, it’s not personal advice. All investments can fall as well as rise in value, so you could get back less than you put in. If you’re not sure what to do, seek advice.

This website is issued by Hargreaves Lansdown Asset Management Limited (company number 1896481), which is authorised and regulated by the Financial Conduct Authority with firm reference 115248.

The Active Savings service is provided by Hargreaves Lansdown Savings Limited (company number 8355960). Hargreaves Lansdown Savings Limited is authorised and regulated by the Financial Conduct Authority (firm reference number 915119). Hargreaves Lansdown Savings Limited is authorised by the Financial Conduct Authority under the Electronic Money Regulations 2011 with firm reference 901007 for the issuing of electronic money.