Semi-retirement

What is semi-retirement?

Rather than stop work completely and fully retire, you could choose to reduce your hours first and gradually phase out working life. This is known as semi-retirement.

Important information - The information on our website isn’t personal advice. If you're not sure what's best for your situation, you should seek financial advice. Money in a pension isn’t usually accessible until age 55 (57 from 2028).

Semi-retirement tips

Semi-retirement is becoming increasingly popular. If you’re hoping to semi-retire, you might find the six tips below helpful.

Tidy up your pensions

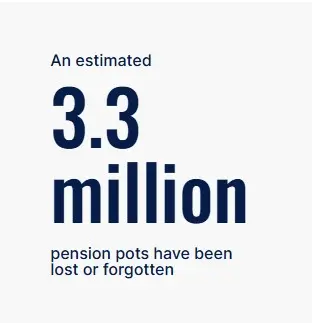

It’s important to know how much pension wealth you’ve built up over the years. It can help you to understand if you can realistically afford to semi-retire, or whether you’re going to have to wait a few more years.

You can find out how much your pensions are worth by digging out old paperwork or contacting your pension providers. If you can’t find any information on your pension and aren’t sure which company it’s with, try the government’s free Pension Tracing Service.

It can be hard to keep track when you’ve got pensions scattered around different companies. To make life easier in the future, you could think about combining any old workplace or private pensions into one place.

Make sure you check for any guarantees or high exit fees before transferring.

Work fewer hours without changing jobs

Flexible working has become the norm for many employees and their employers today. Working fewer hours a week and gradually moving into retirement could be easier than you think.

You can talk to your employer about the possibility of reducing your hours, and have the right to request flexible working. They can refuse, but they must have a valid business reason for doing so. The Citizens Advice Bureau provides online guidance for enquiring about flexible working.

Use pension tax-free cash to top up your income

If you reduce your hours or change jobs it could mean you end up earning less. Luckily, from age 55 (rising to 57 in 2028) your pension can be used to make up for any shortfalls as you settle into new retirement spending and lifestyle habits.

When you access your pension you can normally take up to 25% tax free (up to a maximum of £268,275). This could be used to help supplement any drop in income. How much tax-free cash you get will depend on how and when you decide to take it. Pension drawdown is one option that allows pension savers to access their tax-free cash whilst keeping the rest invested. Just remember, investments can fall as well as rise in value, so you could get back less than you put in.

What you do with your pension is an important decision that you might not be able to change. You should check you're making the right decision for your circumstances and that you understand all your options and their risks. The government's free and impartial Pension Wise service can help you and we can offer you advice if you’d like it.

You can still pay into your pension but be careful if you’ve taken money out

If you’ve got a workplace pension and you reduce your hours, you can continue to receive tax efficient pension contributions from your employer (as long as your salary doesn’t drop below the minimum qualifying value), and tax relief on your personal contributions. The amount paid in each month may be less, but you’ll still get these benefits. Or you can contribute to a private pension and just benefit from tax relief.

Just be aware, if you take a taxable income from your pension through drawdown or as an Uncrystallised Funds Pension Lump Sum (UFPLS) you’ll normally trigger something known as the Money Purchase Annual Allowance (MPAA). This means contributions to all your Money Purchase Pensions are limited to £10,000 each tax year.

If you just take your tax-free cash you won’t trigger the MPAA, but you’ll need to be aware of tax-free cash recycling rules. Pension and tax rules can change and benefits will depend on your circumstances.

You could delay your State Pension

If you’re still working when you reach State Pension age, you might not need it straight away. You can delay payments if you think you won’t need them. For every nine weeks you defer, the government will increase your payments by 1%. This could give you around 5.8% extra a year.

If you’re due to get £241.30 a week when you reach State Pension age but choose to defer it by a year, you'll get an extra £14 a week.

You can delay payments from a defined benefit (e.g. final salary) pension too. Most of these schemes will increase the amount you receive each year if you do defer. Your scheme provider can tell you how much more this will be.

If you delay taking your State Pension or final salary pension you will miss out on income in the meantime. You should weigh up the potential costs and benefits before deciding what to do.

Choose the right time to buy an annuity

If you’re happy to keep your pension invested, you might not benefit from buying an annuity straight away, particularly if you plan to semi-retire.

Throughout retirement your income needs will probably change. In the early years it's possible you’ll want a more flexible income, and in the later years you might be after more security.

A secure income is still really important in retirement. But a good time to look at buying an annuity is when you give up work altogether. You’ll no longer have an income stream from your earnings to cover your essential bills, and an annuity can help cover these.

Rates tend to be higher with age, especially for people with medical conditions. With every year you get older you could get a higher annuity income. Although annuity rates change all the time, so there’s no guarantee the rate you get in the future will be higher than the rate you could get now.

Your annuity rate also depends on the annuity features and options you select, so it’s important to choose your options carefully. Once set up you can’t normally change the contract.

Semi-retirement guide

More detailed information and useful tips.

Expert support and advice

Expert support and advice

Guidance from Pension Wise

Pension Wise is a free government service for people getting ready to receive a UK defined contribution pension (this could be a personal or workplace pension).

It offers impartial guidance on pension types, how to access savings, and the tax implications of each option.

Helpdesk support

Our Bristol-based helpdesk are here for you six days a week. Our friendly and knowledgeable team are ready to answer your questions no matter how big or small.

Please contact us or schedule a callback at your convenience.

Advice on your retirement plans

Our financial advisers can help you develop a retirement income strategy, ensuring that your investments align with your goals.

They'll advise you on the best time and methods for accessing your pension.