HL SELECT UK GROWTH SHARES

New Holdings

Fund changes

HL SELECT UK GROWTH SHARES

Fund changes

Charlie Huggins (CFA) - Fund Manager

16 April 2018

Back in February we wrote to investors with news that Fidessa had agreed to be acquired by Temenos. We have since sold our shares from the HL Select UK Growth fund.

We sold at a price of £37.10, marking a healthy return from our initial investment on the day the fund launched (1 December 2016), when we paid an average price of £22.53. In the months that followed, we bought more at prices ranging from £21.82 to £24.66. And in total, from buying to selling these shares in Fidessa, the fund has received 93.5p in dividends from each share held.

Since we exited the position, a couple of other bidders have come forward and the price has risen further, to just above the £40 level. While it would have been nice to capture this additional bounce, selling now, rather than having to wait for these discussions to conclude, has meant we’ve been able to redeploy the proceeds quickly, taking advantage of recent share price weakness to add two high quality companies to the portfolio.

We used the Fidessa proceeds to purchase Rentokil, the pest control specialist, and Alfa Financial Software; building around a 2.5% position in each. Full rationales for these purchases are available on the portfolio breakdown page.

To choose two more disparate companies from an operational perspective would have been a challenge - one catches rats and replaces soap dispensers for a living, the other designs very high tech software systems to help vehicle and equipment manufacturers, banks and finance companies to run their leasing activities.

However, they actually share quite a lot in common, including:

We like companies with these characteristics because they tend to have greater control of their own destiny. If we can find them in different industries, meaning they’re exposed to different trends and external conditions, then all the better. That way we can build a portfolio that is both attractively positioned, yet resilient and not all facing in the same direction.

We don't mind paying the right price for quality, because great companies can compound their earnings, far out into the future. However, we try not to overpay. That may sound like a contradiction, but perhaps these examples will help to illustrate our approach.

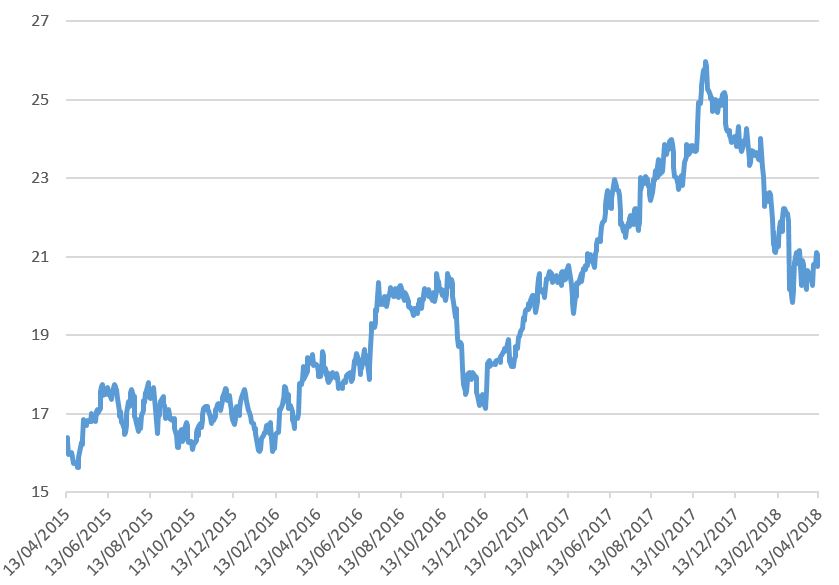

Having disposed of a number of low quality divisions, Rentokil’s prospects have been transformed. Unfortunately, we aren’t the only investors to have noticed. The valuation has steadily risen in recent years, with the price to earnings ratio (P/E) peaking at around 26x in October 2017.

The shares then started to de-rate (in other words, the valuation started to fall) with full year results on 1 March continuing this trend. The numbers themselves were fine, but the company warned that currency headwinds in 2018 will be a little greater than that market had expected. This gave us the opportunity to buy in to the business on a P/E of 20x, which we believe is a much more reasonable valuation.

Past performance is not a guide to the future. Source: Bloomberg 06/07/2017 - 13/04/2018

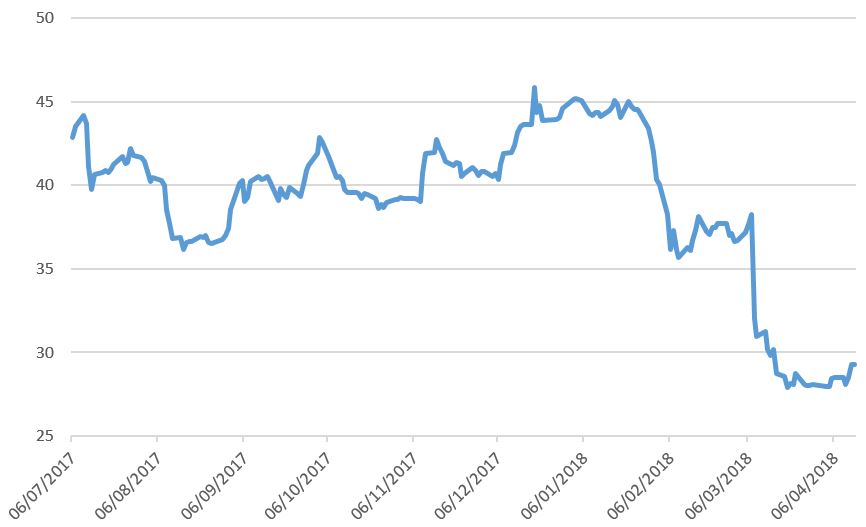

Alfa Financial Software came to market in May 2017. We looked at it very closely before it listed and liked what we saw, but felt the valuation left very little room for disappointment. We also wanted a bit more time to get to know the business.

The shares immediately rose to a big premium and stayed there for several months, commanding a P/E in the early 40s. Maiden results in March were badly received by the market, and the share price tumbled. We felt the problems lay more with the level of market expectations than the company’s underlying performance, so we took the decision to invest.

Past performance is not a guide to the future. Source: Bloomberg 06/07/2017 - 13/04/2018

More about HL Select UK Growth Shares

Please read the Key Investor Information Document before you invest.

Important information: Investments can go down in value as well as up, so you might get back less than you invest. If you are unsure of the suitability of any investment for your circumstances please contact us for advice. Once held in a SIPP money is not usually accessible until age 55 (rising to 57 in 2028).

The maximum you can invest into an ISA in this tax year 2025/2026 is £20,000. Tax rules can change and the value of any benefits depends on individual circumstances.

Invest in an ISAYou can place a deal online now or top up an existing account first, using your debit card.